Company Coverage

Beng Kuang Marine (BKM SP): Strong FPSO Contract Wins Underappreciated By The Market

BUY (MAINTAINED)

Current price:

Target price:

Upside:

S$0.49

S$0.75

+53.1%

Analyst

Analyst

Sidebar Card

Highlights

- ASOM has secured two FPSO life extension contracts worth US$28.6m (~S$36.6m), lifting BKM's pro forma orderbook to approximately S$92.5m.

- We view this positively as the awards validate ASOM's West Africa pipeline, with BKM now capturing 100% of ASOM’s post-consolidation earnings.

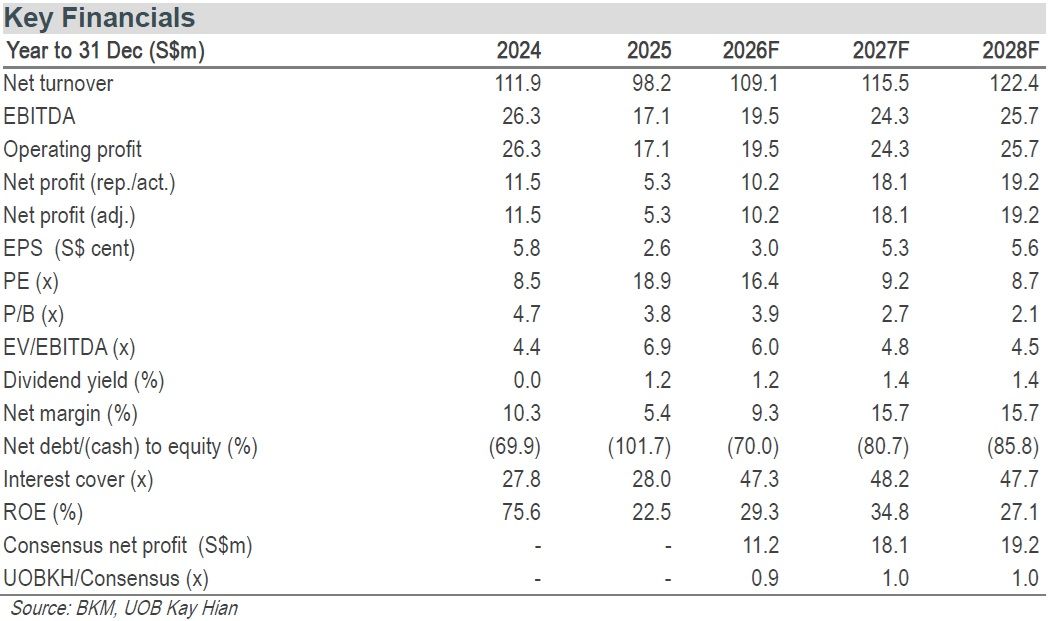

- Maintain BUY with an unchanged target price of S$0.75, pegged to 14x 2027F PE. The recent share price correction of about 20% and attractive 7x 2027 ex-cash PE present a good buying opportunity.

Analysis

- Two new life extension purchase orders of US$28.6m. Beng Kuang Marine’s (BKM) wholly-owned subsidiary, Asian Sealand Offshore and Marine (ASOM), has secured two new purchase orders with an aggregate contract value of approximately US$28.6m (~S$36.7m) for FPSO life extension projects on two FPSOs operating in West Africa. The contracts, valued at approximately US$13.2m and US$15.4m respectively, are expected to be executed over the next 12 months. The recent consolidation of ASOM would also allow the group to fully capture the earnings contribution from these contracts. The new orders are expected to significantly enhance revenue visibility and earnings for FY26-27, strengthen orderbook growth, and further reinforce ASOM's position as the group's primary earnings driver under its BKM 2.0 strategy. In addition, successful execution of these initial tank service works could position ASOM favourably for subsequent phases of the FPSO life extension programmes, providing potential opportunities for additional contract awards over the coming years.

- Contracts secured continue to strengthen 2026-27 earnings visibility. Following BKM’s 1Q26 contract update, which reported approximately S$51.2m of secured FY26 revenue and an orderbook of S$55.9m, the recent two new FPSO life extension purchase orders worth US$28.6m (~S$36.6m) lift the group's total orderbook to about S$92.5m, significantly enhancing revenue visibility over the next 12 months. The latest awards further validate management's expectations of additional West Africa FPSO-related opportunities and reinforce ASOM's role as the group's key earnings engine under the BKM 2.0 strategy. The group's revenue base remains increasingly anchored by ASOM's recurring offshore maintenance activities, complemented by NEI's fabrication projects and IOE's equipment business, providing a more diversified and durable earnings profile.

Stock Impact

- Strong business momentum expected in 2Q26. BKM highlighted stronger business momentum in April and May and expects additional contract awards in 2Q26. In addition, BKM is currently executing five FPSO contracts in Guyana, with a potential pipeline of four more FPSO projects in Central America, which is expected to significantly strengthen FPSO-related revenue contributions in the near term. To support the anticipated ramp-up in operations, deployed FPSO headcount is projected to increase from around 30 currently to approximately 120 between June and September, while the company also plans to deploy a floatel by Sep 26 to support its FPSO operations in Angola.

- Expect higher revenue recognition in 2H26. BKM’s proposed acquisition of the remaining stake in ASOM is expected to be completed by end-Jun 26. The transaction is expected to significantly boost BKM's 2H26 revenue and is also earnings-accretive, enabling the group to fully capture ASOM’s high-margin earnings while strengthening its core engineering segment. This is also in line with the company’s strategy to shift towards an asset-light business model under BKM 2.0, given the nature of ASOM’s business.

- Continued shareholders’ confidence in BKM. BKM’s founder recently divested part of his stake, attracting strong demand from institutional and reputable investors. At the same time, management reinforced confidence by increasing their shareholdings. We view this transaction positively, as it strengthens the shareholder base and enhances alignment between management and investors as the group advances its BKM 2.0 strategy.

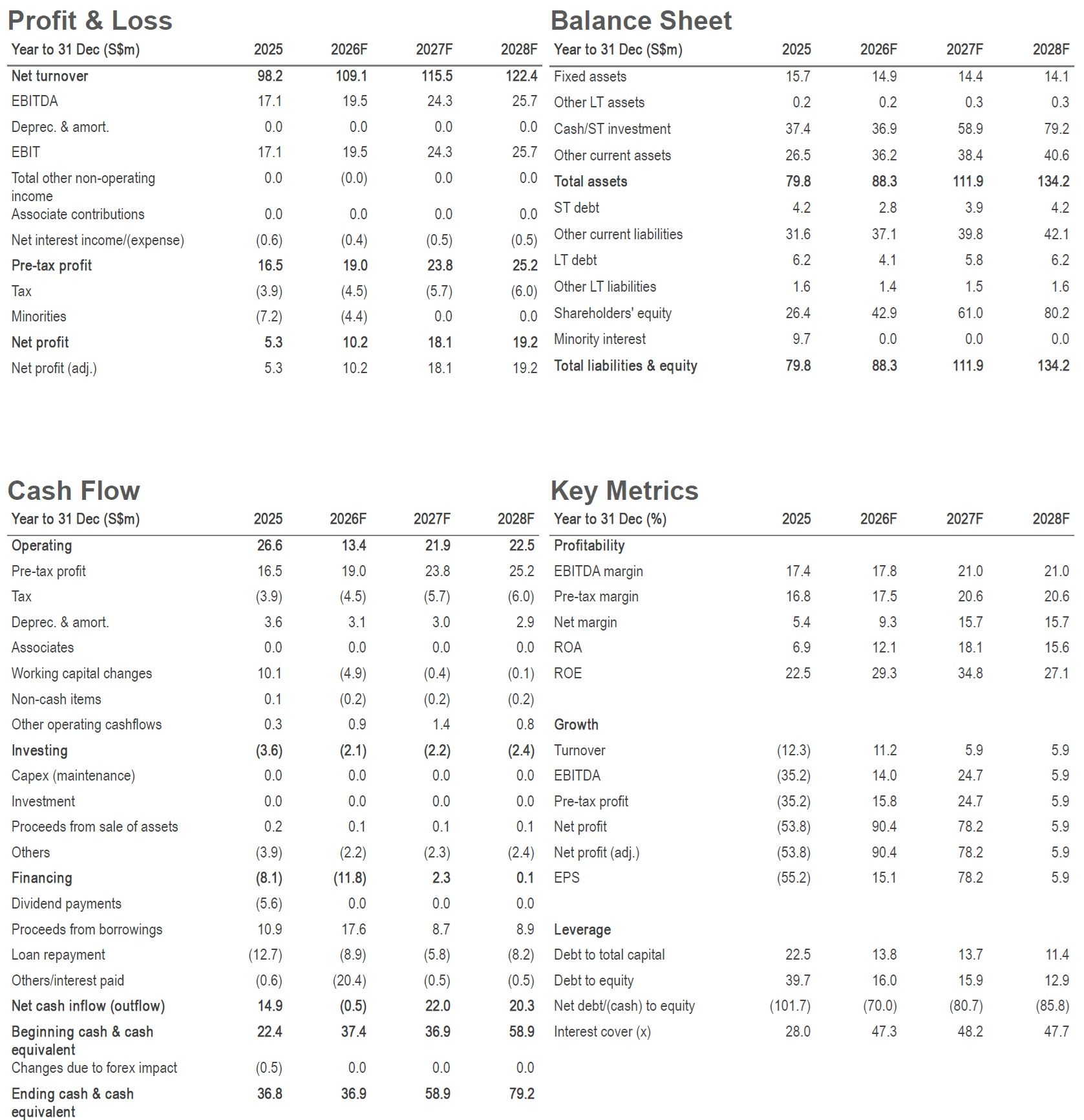

- Healthy balance sheet position. BKM remains in a net cash position of S$26.9m as at end-25 with little debt. BKM has been focused on paying down its debt, backed by its strong cash flow from operations of S$26.6m as at end-25. This strong balance sheet is likely to strengthen further as BKM continues to shift towards an asset-light operating model under its BKM 2.0 strategy, positioning the company well to capitalise on any opportunities amid strong industry tailwinds.

Valuation/Recommendation

- Maintain BUY with an unchanged target price of S$0.75, implying 53.1% upside. Our target price is pegged to 14.0x 2027F PE, +1.5SD above historical averages, and we expect re-rating to continue as BKM continues to gain traction from participation of more institutional and strategic shareholders. This also represents a discount to peers’ average despite BKM’s market position and higher profitability following the consolidation of ASOM.

- BKM currently trades around 9.2x 2027F PE, below peers’ average of 12.5x 2027F PE, highlighting BKM’s undervaluation. We believe its strong fundamentals, underpinned by a superior ROE of 38.8% vs the industry average of 17.3% and a strong net cash position, continue to support the case for valuation re-rating. Full-year consolidation of ASOM in 2027 is also expected to boost BKM’s profitability significantly.

Earnings Revision/Risk

- No changes to our earnings forecasts.

Share Price Catalyst

- Higher revenue and profit recognition from ASOM following consolidation.

- Winning of more high-value FPSO extension of life jobs.

Highlights

- ASOM has secured two FPSO life extension contracts worth US$28.6m (~S$36.6m), lifting BKM's pro forma orderbook to approximately S$92.5m.

- We view this positively as the awards validate ASOM's West Africa pipeline, with BKM now capturing 100% of ASOM’s post-consolidation earnings.

- Maintain BUY with an unchanged target price of S$0.75, pegged to 14x 2027F PE. The recent share price correction of about 20% and attractive 7x 2027 ex-cash PE present a good buying opportunity.

Analysis

- Two new life extension purchase orders of US$28.6m. Beng Kuang Marine’s (BKM) wholly-owned subsidiary, Asian Sealand Offshore and Marine (ASOM), has secured two new purchase orders with an aggregate contract value of approximately US$28.6m (~S$36.7m) for FPSO life extension projects on two FPSOs operating in West Africa. The contracts, valued at approximately US$13.2m and US$15.4m respectively, are expected to be executed over the next 12 months. The recent consolidation of ASOM would also allow the group to fully capture the earnings contribution from these contracts. The new orders are expected to significantly enhance revenue visibility and earnings for FY26-27, strengthen orderbook growth, and further reinforce ASOM's position as the group's primary earnings driver under its BKM 2.0 strategy. In addition, successful execution of these initial tank service works could position ASOM favourably for subsequent phases of the FPSO life extension programmes, providing potential opportunities for additional contract awards over the coming years.

- Contracts secured continue to strengthen 2026-27 earnings visibility. Following BKM’s 1Q26 contract update, which reported approximately S$51.2m of secured FY26 revenue and an orderbook of S$55.9m, the recent two new FPSO life extension purchase orders worth US$28.6m (~S$36.6m) lift the group's total orderbook to about S$92.5m, significantly enhancing revenue visibility over the next 12 months. The latest awards further validate management's expectations of additional West Africa FPSO-related opportunities and reinforce ASOM's role as the group's key earnings engine under the BKM 2.0 strategy. The group's revenue base remains increasingly anchored by ASOM's recurring offshore maintenance activities, complemented by NEI's fabrication projects and IOE's equipment business, providing a more diversified and durable earnings profile.

Stock Impact

- Strong business momentum expected in 2Q26. BKM highlighted stronger business momentum in April and May and expects additional contract awards in 2Q26. In addition, BKM is currently executing five FPSO contracts in Guyana, with a potential pipeline of four more FPSO projects in Central America, which is expected to significantly strengthen FPSO-related revenue contributions in the near term. To support the anticipated ramp-up in operations, deployed FPSO headcount is projected to increase from around 30 currently to approximately 120 between June and September, while the company also plans to deploy a floatel by Sep 26 to support its FPSO operations in Angola.

- Expect higher revenue recognition in 2H26. BKM’s proposed acquisition of the remaining stake in ASOM is expected to be completed by end-Jun 26. The transaction is expected to significantly boost BKM's 2H26 revenue and is also earnings-accretive, enabling the group to fully capture ASOM’s high-margin earnings while strengthening its core engineering segment. This is also in line with the company’s strategy to shift towards an asset-light business model under BKM 2.0, given the nature of ASOM’s business.

- Continued shareholders’ confidence in BKM. BKM’s founder recently divested part of his stake, attracting strong demand from institutional and reputable investors. At the same time, management reinforced confidence by increasing their shareholdings. We view this transaction positively, as it strengthens the shareholder base and enhances alignment between management and investors as the group advances its BKM 2.0 strategy.

- Healthy balance sheet position. BKM remains in a net cash position of S$26.9m as at end-25 with little debt. BKM has been focused on paying down its debt, backed by its strong cash flow from operations of S$26.6m as at end-25. This strong balance sheet is likely to strengthen further as BKM continues to shift towards an asset-light operating model under its BKM 2.0 strategy, positioning the company well to capitalise on any opportunities amid strong industry tailwinds.

Valuation/Recommendation

- Maintain BUY with an unchanged target price of S$0.75, implying 53.1% upside. Our target price is pegged to 14.0x 2027F PE, +1.5SD above historical averages, and we expect re-rating to continue as BKM continues to gain traction from participation of more institutional and strategic shareholders. This also represents a discount to peers’ average despite BKM’s market position and higher profitability following the consolidation of ASOM.

- BKM currently trades around 9.2x 2027F PE, below peers’ average of 12.5x 2027F PE, highlighting BKM’s undervaluation. We believe its strong fundamentals, underpinned by a superior ROE of 38.8% vs the industry average of 17.3% and a strong net cash position, continue to support the case for valuation re-rating. Full-year consolidation of ASOM in 2027 is also expected to boost BKM’s profitability significantly.

Earnings Revision/Risk

- No changes to our earnings forecasts.

Share Price Catalyst

- Higher revenue and profit recognition from ASOM following consolidation.

- Winning of more high-value FPSO extension of life jobs.

BUY (MAINTAINED)

Current price:

Target price:

Upside:

S$0.49

S$0.75

+53.1%

Analyst

Analyst

Sidebar Card

IMPORTANT NOTICE - DISCLOSURES AND DISCLAIMERS

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/df64a6ea-7980-447c-ae9e-fd19b93257dc, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.