Overnight Markets

Today’s Must-Know News

- Hawkish Fed jolts markets. S&P 500 sank 1.21% to 7,420.10 & US 2-year Treasury yields jumped > 13-bps to 4.184% Wednesday. Fed funds futures fully priced a 25-bps hike by October after the first Fed meeting under Chair Kevin Warsh signalled rates could rise again. SpaceX (SPCX -4.95%) fell for the first time since IPO. Gold (XAU -1.71%) fell to USD4,256.93/oz as dollar (DXY +0.85%) rose. Meanwhile, S&P 500 futures rose 0.6%.

- Microsoft scales China AI sales. Microsoft (MSFT -3.79%) is expanding AI offerings in China by selling OpenAI-powered models to local firms, with ByteDance spending over USD 1bn annually on AI and cloud services. MSFT is our Core Recommendation.

- US backs Venezuela grid revival via GE Vernova deal. GE Vernova (GEV +6.77%) signed an MOU with Venezuela’s state utility Corpoelec to expand power generation under a US-backed stabilisation plan. The deal targets about 1GW within two years & more than 5GW within four years. GEV is our Core Recommendation.

- ARK adds LLY & COIN, rotates out of HOOD and ROKU. Eli Lilly (LLY -0.94%) was the largest buy by ARK Invest, which purchased 41,138 shares via ARKK (ARKK -0.75%) and ARKG (ARKG +0.46%) ETFs for about USD 46.2mn. LLY is our Core Recommendation.

- No Wealth Daily tomorrow (Friday) – HK public holiday.

| Trader's Corner (Details on Page 6-7) | ||||

| Ticker | Name | Rec. | Support Levels | Resistance Levels |

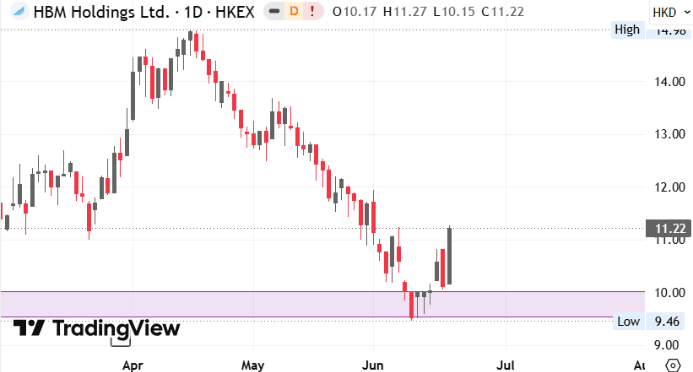

| 2142.HK | HBM | - | HK$10.06/$9.46 | HK$13.68/$14.98 |

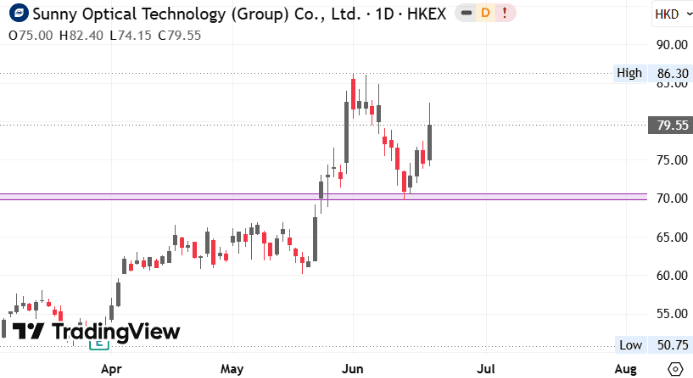

| 2382.HK | Sunny Optical | - | HK$73.80/$69.80 | HK$86.30/$90.05 |

| CR = Core Recommendation; TB = Trading Buy | ||||

| Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 1392.HK | HQVT | Technology | Jun 22 |

| 6067.HK | Senior Material | Industrials | Jun 23 |

| 6132.HK | HJ Science-B | Healthcare | Jun 23 |

| 2335.HK | Micot Pharma-B | Healthcare | Jun 24 |

| 6106.HK | Seer Tech | Technology | Jun 24 |

| 1688.HK | Lingyi iTech | Technology | Jun 26 |

| 1956.HK | Wenge AI | Technology | Jun 26 |

| 2272.HK | Keytop Parking | Discretionary | Jun 26 |

| 3661.HK | SG Micro | Discretionary | Jun 26 |

| 6228.HK | Merdekagold-DRS | Materials | Jun 26 |

| 9630.HK | CFMEE | Technology | Jun 26 |

Americas

- G7 targets critical minerals de-risking. The G7 agreed to build a coordinated critical minerals alliance to cut reliance on a single supplier to below 60% by 2030, starting with lithium and nickel. The plan includes IEA-linked monitoring and stockpiling coordination to secure rare earths and defence-critical materials amid supply disruption risks. (Reuters)

- AI leaders push G7 coordination. Dario Amodei (Anthropic), Sam Altman (OpenAI) & Demis Hassabis (Alphabet (GOOGL -2.53%)) urged G7 leaders to avoid fragmented AI regulation and coordinate on model safety and cyber defence. The group made the comments at a meeting attended by President Trump, calling for stronger US-led collaboration on AI governance. (Bloomberg / FT) GOOGL is our Trading Buy.

- OpenAI burn rate highlights AI investment costs. OpenAI reportedly burned through USD 3.7 bn in 1Q26, exceeding half of its USD 5.7 bn revenue, underscoring the heavy spending required to scale advanced AI model. The report comes after OpenAI confidentially filed for a US IPO that could value the firm at up to USD 1 tn. (Reuters / The Information)

- US grid rules raise data center costs. FERC is preparing guidance that could speed up data center grid connections but shift more upgrade costs onto hyperscalers including Amazon (AMZN -3.46%) amid surging AI-driven electricity demand. (Bloomberg) AMZN is our Core Recommendation.

- Meta AI work leadership exit. Meta (META -5.44%) executive Emily Dalton Smith, who recently took charge of improving the firm’s internal AI tools, is leaving the firm amid a broader AI-driven restructuring. The overhaul, which includes workforce reductions and increased automation initiatives, has drawn criticism from some employees. (Reuters) META is our Core Recommendation.

- Apple flags price pressure from memory costs. Apple (AAPL -1.1%) CEO Tim Cook said price increases may be unavoidable as AI-driven demand for DRAM and storage tightens supply and lifts component costs. He added that memory is being diverted to AI servers, worsening shortages for consumer devices, while Apple will use its balance sheet to secure supply without building its own fabs. Separately, Apple is developing a second-generation iPhone Air for spring 2027. (Bloomberg / Reuters / WSJ)

- Bezos sees AI-driven labour squeeze. Amazon’s (AMZN -3.46%) Jeff Bezos said AI will boost productivity and lower creation barriers, potentially leading to labour shortages rather than unemployment as output expands faster than job displacement. He added that AI will enable more innovation even as firms cut roles on efficiency gains and concerns over AI-driven job losses rise. (Bloomberg) AMZN is our Core Recommendation.

- FTC probe raises legal risk for Amazon. Amazon (AMZN -3.46%) could face an FTC lawsuit and potential civil penalties over allegations it misled advertisers on pricing and auction practices, according to a Bloomberg report. The investigation is part of a broader FTC review of online advertising disclosures that also involves Alphabet's Google (GOOGL -2.53%). (Reuters) AMZN is our Core Recommendation & GOOGL is our Trading Buy.

- Amazon backs world model startup. Amazon (AMZN -3.46%) participated in Odyssey's USD 310 mn funding round, which valued the AI startup at USD 1.45 bn, as it bets on world models that simulate physical environments and could expand demand for its Trainium chips. AMD Ventures (AMD +1.02%) & Alphabet’s (GOOGL -2.53%) GV also participated in the fund raising. (Reuters) AMZN is our Core Recommendation & GOOGL is our Trading Buy.

- UK AI adoption hits tipping point. Alphabet’s (GOOGL -2.53%) Google Cloud’s Maureen Costello said UK AI adoption has reached a “tipping point” as firms shift to large-scale deployment and see productivity gains. Meanwhile, the UK CMA ordered Google to improve search transparency, complaints handling and data portability to curb its >90% market dominance with compliance required in 3–6 months. (Reuters) GOOGL is our Trading Buy.

- ASML eyes Musk-driven chip upside. Elon Musk’s Terafab project could lift semiconductor equipment demand, with ASML (ASML NA +4.1%) CEO Christophe Fouquet citing it as a potential upside driver if large-scale chip capacity plans proceed without supply constraints. ASML is monitoring timing and ramp speed of such projects while ensuring it can meet rising advanced chip demand. (Bloomberg)

- Exxon signs South Africa LNG supply deal. Exxon Mobil (XOM -0.79%) has signed a preliminary agreement to supply LNG to South Africa's planned Zululand Energy Terminal, which is set to become the country's first LNG import facility. The project supports South Africa's transition away from coal and plans to develop a competitive domestic gas market. (Reuters)

Greater China

- AI gains offset economic concerns. CSI 300 edged up 0.1% while HSI fell 0.4% on Wednesday, as strength in AI and semiconductor shares countered weakness in consumer and financial stocks. Investors weighed soft China retail sales data and regulatory comments on financial risk management amid ongoing economic restructuring. (Reuters)

- China has drafted rules to curb food delivery subsidy wars. China has banned long-term below-cost competition and forced greater transparency. (BABA -3.18%; 9988.HK -0.09%; 3690.HK -1.2%; JD -1.66%; 9618.HK -0.45%). (Bloomberg) 9988.HK is our Core Recommendation.

- US delays blacklist expansion on China firms. The US has reportedly held off adding China's DeepSeek and memory chipmaker CXMT to its Entity List, along with more than 100 other companies previously flagged as national security risks, as Washington seeks to avoid escalating tensions with Beijing. The delay has raised concerns that sensitive US technology could continue reaching entities viewed as strategic rivals. (Reuters)

- China EV brands go premium overseas. Chinese automakers including Geely's (0175.HK -2.76%) Zeekr, BYD's (1211.HK -2.56%) Denza, Chery, GAC (2238.HK -2.93%), Hongqi (1378.HK -1.98%), & SAIC’s (SAIC -1.97%) MG Motor are expanding into right-hand-drive markets with premium EVs targeting rivals like Toyota (7203 JP -1.32%). The push reflects rising EV adoption and stronger overseas demand driving a shift up the value chain. (Reuters) 0175.HK is our Core Recommendation.

- Tencent Cloud advances embodied AI initiative. Tencent (0700.HK -0.45%) said its cloud unit partnered with Beijing Wuwen Zhixing Technology to build physical AI infrastructure and accelerate embodied intelligence applications. The collaboration will combine Tencent's Hunyuan models with Wuwen Zhixing's AI data platform and simulation technologies. (AAStocks) 0700.HK is our Core Recommendation.

- Hong Kong IPO momentum accelerates. Six companies launched Hong Kong share offerings on Wednesday seeking to raise up to HKD 19.8 bn, led by Lingyi iTech (1688.HK), as improving market sentiment fuels listing activity. Hong Kong IPO and secondary listing proceeds have more than doubled yoy in 2026, supported by strong demand for AI and new-economy companies. (Reuters)

- China speeds AI IPO push. Shanghai Stock Exchange and regulators are expanding IPO support for “future industry” startups, including large language model firms, as China targets AI, quantum computing and fusion energy amid US–China tech competition. STAR Market rule changes aim to ease listings for large-model AI companies to accelerate innovation financing. (Reuters)

- JD Cloud integrates latest GLM AI model. JD.com (JD -1.66%; 9618.HK -0.45%) said its JD Cloud JoyBuilder platform has integrated Knowledge Atlas' (2513.HK +12.62%) flagship open-source GLM-5.2 model, enhancing inference throughput and response efficiency through proprietary optimization technologies. The integration is expected to provide developers and enterprises with faster and more stable AI model services. (Reuters)

- China expands yuan liquidity support. China's central bank launched a new repurchase agreement facility to provide yuan liquidity to overseas central bank-type institutions, allowing them to pledge eligible Chinese securities as collateral as Beijing seeks to expand the yuan's global use and strengthen liquidity management. (Reuters)

- China approves active ETF rollout. China's regulator will support the launch of actively managed exchange-traded funds in Shanghai and Shenzhen, broadening investment options beyond index-tracking products to meet diversification demand and promote innovation in the mutual fund industry. (Bloomberg)

- Kling AI seeks major funding round. Kuaishou (1024.HK +7.34%) is in talks with General Atlantic to lead the first financing round for its Kling AI unit ahead of a potential IPO, with the business aiming to raise more than USD 2 bn at a post-money valuation of about USD 18 bn. (Bloomberg)

Asia ex. China

- Japan firms flag slow Iran shock recovery. Nearly half of Japanese companies expect more than six months to normalize operations after the Iran conflict, citing energy disruption and Strait of Hormuz risks, according to a Reuters survey. 56% also said AI is already reshaping hiring, with weaker office demand but stronger need for AI-skilled workers. (Reuters)

- SK Hynix advances next-generation AI memory. SK Hynix (000660.KS +3.47%) has shipped samples of its latest 12-layer HBM4E chips to major customers, offering more than 20% better power efficiency and faster performance than previous models. The move strengthens its position in the AI memory market, where it is a key supplier to Nvidia (NVDA -1.33%). (Reuters) NVDA is our Core Recommendation.

- CSE Global remains supported by strong orderbook. CSE Global (CSE SP +0.04%) said its response to SGX RegCo's queries reflects board-refresh matters rather than operational issues. With a robust SGD 716 mn orderbook as of 1Q26, the company expects a softer 1H26 due to new facility start-up costs, while maintaining solid long-term growth prospects. (UOB Kay Hian Institutional Research)

EMEA and Others

- European stocks gain on trade optimism. STOXX 600 rose 0.52% on Wednesday as investors focused on signals from the G7 summit and growing optimism over a potential EU-India free trade agreement. Germany's DAX gained 0.1% and the UK's FTSE 100 added 0.14%, while France's CAC 40 slipped 0.2%. (Reuters)

- Europe pushes for AI sovereignty. Technology sovereignty is set to dominate discussions at the G7 and VivaTech this week as European policymakers seek to reduce dependence on US AI infrastructure and models. Recent US restrictions on advanced AI exports have highlighted Europe's reliance on foreign cloud, chip and AI providers, including IBM (IBM -3.12%). (Reuters)

- BMW warning highlights auto sector pressures. BMW (BMW GR -3.33%) shares fell to their lowest level since 2020 after the carmaker cut its 2026 profit outlook, citing weakness in China's auto market and pressures linked to the Iran conflict. The warning also weighed on European peers including Volkswagen (VOW GR -1.57%) and Mercedes-Benz (MBG GR -1.9%). (Reuters)

- Qatar stake complicates Volkswagen defence deal. Volkswagen (VOW GR -1.57%) is facing complications in plans to partner with Israeli defence firm Rafael at its underutilised Osnabrueck plant, as major shareholder Qatar Investment Authority has reportedly raised concerns over the discussions. The issue could delay Volkswagen's efforts to repurpose excess manufacturing capacity amid weak European auto demand. (Reuters)

- Stellantis explores new partnership opportunities. Stellantis (STLAM

IM -3.25%) is in talks with potential partners for two additional manufacturing deals in Italy, including one involving its luxury Maserati brand, as part of efforts to strengthen technology and product development. The automaker is also expanding existing collaborations with Leapmotor (9863.HK -0.82%) and Dongfeng Motor under its long-term growth strategy. (Reuters)

TRADERS’ CORNER

Source: TradingView | HBM (2142.HK)

Last Price: HK$11.22 Support Levels: HK$10.06 (-10.3%)/ HK$9.46 (-15.7%) Resistance Levels: HK$13.68 (+21.9%)/ HK$14.98 (+33.5%) |

Our Technical View

- Price action has staged a decisive rebound from a major weekly resistance-turned-support zone, validating the long-term structural floor.

- This structural defence is supported by the RSI trending upward toward the neutral 50 level.

- Provided the asset maintains its footing above this critical weekly demand floor, the current framework points toward a high-probability continuation into higher territory.

Source: TradingView | Sunny Optical (2382.HK)

Last Price: HK$79.55 Support Levels: HK$73.80 (-7.2%)/ HK$69.80 (-12.3%) Resistance Levels: HK$86.30 (+8.5%)/ HK$90.05 (+13.2%) |

Our Technical View

- Following a clean bounce off its resistance-turned-support zone, the asset has renewed its upward expansion.

- Momentum has officially shifted in favour of the bulls as the RSI clears its neutral midline and trends upward.

- Provided this underlying buying velocity persists, the path of least resistance points toward an impending challenge of the recent peak, clearing the path for further structural upside.

Today’s Must-Know News

- Hawkish Fed jolts markets. S&P 500 sank 1.21% to 7,420.10 & US 2-year Treasury yields jumped > 13-bps to 4.184% Wednesday. Fed funds futures fully priced a 25-bps hike by October after the first Fed meeting under Chair Kevin Warsh signalled rates could rise again. SpaceX (SPCX -4.95%) fell for the first time since IPO. Gold (XAU -1.71%) fell to USD4,256.93/oz as dollar (DXY +0.85%) rose. Meanwhile, S&P 500 futures rose 0.6%.

- Microsoft scales China AI sales. Microsoft (MSFT -3.79%) is expanding AI offerings in China by selling OpenAI-powered models to local firms, with ByteDance spending over USD 1bn annually on AI and cloud services. MSFT is our Core Recommendation.

- US backs Venezuela grid revival via GE Vernova deal. GE Vernova (GEV +6.77%) signed an MOU with Venezuela’s state utility Corpoelec to expand power generation under a US-backed stabilisation plan. The deal targets about 1GW within two years & more than 5GW within four years. GEV is our Core Recommendation.

- ARK adds LLY & COIN, rotates out of HOOD and ROKU. Eli Lilly (LLY -0.94%) was the largest buy by ARK Invest, which purchased 41,138 shares via ARKK (ARKK -0.75%) and ARKG (ARKG +0.46%) ETFs for about USD 46.2mn. LLY is our Core Recommendation.

- No Wealth Daily tomorrow (Friday) – HK public holiday.

| Trader's Corner (Details on Page 6-7) | ||||

| Ticker | Name | Rec. | Support Levels | Resistance Levels |

| 2142.HK | HBM | - | HK$10.06/$9.46 | HK$13.68/$14.98 |

| 2382.HK | Sunny Optical | - | HK$73.80/$69.80 | HK$86.30/$90.05 |

| CR = Core Recommendation; TB = Trading Buy | ||||

| Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 1392.HK | HQVT | Technology | Jun 22 |

| 6067.HK | Senior Material | Industrials | Jun 23 |

| 6132.HK | HJ Science-B | Healthcare | Jun 23 |

| 2335.HK | Micot Pharma-B | Healthcare | Jun 24 |

| 6106.HK | Seer Tech | Technology | Jun 24 |

| 1688.HK | Lingyi iTech | Technology | Jun 26 |

| 1956.HK | Wenge AI | Technology | Jun 26 |

| 2272.HK | Keytop Parking | Discretionary | Jun 26 |

| 3661.HK | SG Micro | Discretionary | Jun 26 |

| 6228.HK | Merdekagold-DRS | Materials | Jun 26 |

| 9630.HK | CFMEE | Technology | Jun 26 |

Americas

- G7 targets critical minerals de-risking. The G7 agreed to build a coordinated critical minerals alliance to cut reliance on a single supplier to below 60% by 2030, starting with lithium and nickel. The plan includes IEA-linked monitoring and stockpiling coordination to secure rare earths and defence-critical materials amid supply disruption risks. (Reuters)

- AI leaders push G7 coordination. Dario Amodei (Anthropic), Sam Altman (OpenAI) & Demis Hassabis (Alphabet (GOOGL -2.53%)) urged G7 leaders to avoid fragmented AI regulation and coordinate on model safety and cyber defence. The group made the comments at a meeting attended by President Trump, calling for stronger US-led collaboration on AI governance. (Bloomberg / FT) GOOGL is our Trading Buy.

- OpenAI burn rate highlights AI investment costs. OpenAI reportedly burned through USD 3.7 bn in 1Q26, exceeding half of its USD 5.7 bn revenue, underscoring the heavy spending required to scale advanced AI model. The report comes after OpenAI confidentially filed for a US IPO that could value the firm at up to USD 1 tn. (Reuters / The Information)

- US grid rules raise data center costs. FERC is preparing guidance that could speed up data center grid connections but shift more upgrade costs onto hyperscalers including Amazon (AMZN -3.46%) amid surging AI-driven electricity demand. (Bloomberg) AMZN is our Core Recommendation.

- Meta AI work leadership exit. Meta (META -5.44%) executive Emily Dalton Smith, who recently took charge of improving the firm’s internal AI tools, is leaving the firm amid a broader AI-driven restructuring. The overhaul, which includes workforce reductions and increased automation initiatives, has drawn criticism from some employees. (Reuters) META is our Core Recommendation.

- Apple flags price pressure from memory costs. Apple (AAPL -1.1%) CEO Tim Cook said price increases may be unavoidable as AI-driven demand for DRAM and storage tightens supply and lifts component costs. He added that memory is being diverted to AI servers, worsening shortages for consumer devices, while Apple will use its balance sheet to secure supply without building its own fabs. Separately, Apple is developing a second-generation iPhone Air for spring 2027. (Bloomberg / Reuters / WSJ)

- Bezos sees AI-driven labour squeeze. Amazon’s (AMZN -3.46%) Jeff Bezos said AI will boost productivity and lower creation barriers, potentially leading to labour shortages rather than unemployment as output expands faster than job displacement. He added that AI will enable more innovation even as firms cut roles on efficiency gains and concerns over AI-driven job losses rise. (Bloomberg) AMZN is our Core Recommendation.

- FTC probe raises legal risk for Amazon. Amazon (AMZN -3.46%) could face an FTC lawsuit and potential civil penalties over allegations it misled advertisers on pricing and auction practices, according to a Bloomberg report. The investigation is part of a broader FTC review of online advertising disclosures that also involves Alphabet's Google (GOOGL -2.53%). (Reuters) AMZN is our Core Recommendation & GOOGL is our Trading Buy.

- Amazon backs world model startup. Amazon (AMZN -3.46%) participated in Odyssey's USD 310 mn funding round, which valued the AI startup at USD 1.45 bn, as it bets on world models that simulate physical environments and could expand demand for its Trainium chips. AMD Ventures (AMD +1.02%) & Alphabet’s (GOOGL -2.53%) GV also participated in the fund raising. (Reuters) AMZN is our Core Recommendation & GOOGL is our Trading Buy.

- UK AI adoption hits tipping point. Alphabet’s (GOOGL -2.53%) Google Cloud’s Maureen Costello said UK AI adoption has reached a “tipping point” as firms shift to large-scale deployment and see productivity gains. Meanwhile, the UK CMA ordered Google to improve search transparency, complaints handling and data portability to curb its >90% market dominance with compliance required in 3–6 months. (Reuters) GOOGL is our Trading Buy.

- ASML eyes Musk-driven chip upside. Elon Musk’s Terafab project could lift semiconductor equipment demand, with ASML (ASML NA +4.1%) CEO Christophe Fouquet citing it as a potential upside driver if large-scale chip capacity plans proceed without supply constraints. ASML is monitoring timing and ramp speed of such projects while ensuring it can meet rising advanced chip demand. (Bloomberg)

- Exxon signs South Africa LNG supply deal. Exxon Mobil (XOM -0.79%) has signed a preliminary agreement to supply LNG to South Africa's planned Zululand Energy Terminal, which is set to become the country's first LNG import facility. The project supports South Africa's transition away from coal and plans to develop a competitive domestic gas market. (Reuters)

Greater China

- AI gains offset economic concerns. CSI 300 edged up 0.1% while HSI fell 0.4% on Wednesday, as strength in AI and semiconductor shares countered weakness in consumer and financial stocks. Investors weighed soft China retail sales data and regulatory comments on financial risk management amid ongoing economic restructuring. (Reuters)

- China has drafted rules to curb food delivery subsidy wars. China has banned long-term below-cost competition and forced greater transparency. (BABA -3.18%; 9988.HK -0.09%; 3690.HK -1.2%; JD -1.66%; 9618.HK -0.45%). (Bloomberg) 9988.HK is our Core Recommendation.

- US delays blacklist expansion on China firms. The US has reportedly held off adding China's DeepSeek and memory chipmaker CXMT to its Entity List, along with more than 100 other companies previously flagged as national security risks, as Washington seeks to avoid escalating tensions with Beijing. The delay has raised concerns that sensitive US technology could continue reaching entities viewed as strategic rivals. (Reuters)

- China EV brands go premium overseas. Chinese automakers including Geely's (0175.HK -2.76%) Zeekr, BYD's (1211.HK -2.56%) Denza, Chery, GAC (2238.HK -2.93%), Hongqi (1378.HK -1.98%), & SAIC’s (SAIC -1.97%) MG Motor are expanding into right-hand-drive markets with premium EVs targeting rivals like Toyota (7203 JP -1.32%). The push reflects rising EV adoption and stronger overseas demand driving a shift up the value chain. (Reuters) 0175.HK is our Core Recommendation.

- Tencent Cloud advances embodied AI initiative. Tencent (0700.HK -0.45%) said its cloud unit partnered with Beijing Wuwen Zhixing Technology to build physical AI infrastructure and accelerate embodied intelligence applications. The collaboration will combine Tencent's Hunyuan models with Wuwen Zhixing's AI data platform and simulation technologies. (AAStocks) 0700.HK is our Core Recommendation.

- Hong Kong IPO momentum accelerates. Six companies launched Hong Kong share offerings on Wednesday seeking to raise up to HKD 19.8 bn, led by Lingyi iTech (1688.HK), as improving market sentiment fuels listing activity. Hong Kong IPO and secondary listing proceeds have more than doubled yoy in 2026, supported by strong demand for AI and new-economy companies. (Reuters)

- China speeds AI IPO push. Shanghai Stock Exchange and regulators are expanding IPO support for “future industry” startups, including large language model firms, as China targets AI, quantum computing and fusion energy amid US–China tech competition. STAR Market rule changes aim to ease listings for large-model AI companies to accelerate innovation financing. (Reuters)

- JD Cloud integrates latest GLM AI model. JD.com (JD -1.66%; 9618.HK -0.45%) said its JD Cloud JoyBuilder platform has integrated Knowledge Atlas' (2513.HK +12.62%) flagship open-source GLM-5.2 model, enhancing inference throughput and response efficiency through proprietary optimization technologies. The integration is expected to provide developers and enterprises with faster and more stable AI model services. (Reuters)

- China expands yuan liquidity support. China's central bank launched a new repurchase agreement facility to provide yuan liquidity to overseas central bank-type institutions, allowing them to pledge eligible Chinese securities as collateral as Beijing seeks to expand the yuan's global use and strengthen liquidity management. (Reuters)

- China approves active ETF rollout. China's regulator will support the launch of actively managed exchange-traded funds in Shanghai and Shenzhen, broadening investment options beyond index-tracking products to meet diversification demand and promote innovation in the mutual fund industry. (Bloomberg)

- Kling AI seeks major funding round. Kuaishou (1024.HK +7.34%) is in talks with General Atlantic to lead the first financing round for its Kling AI unit ahead of a potential IPO, with the business aiming to raise more than USD 2 bn at a post-money valuation of about USD 18 bn. (Bloomberg)

Asia ex. China

- Japan firms flag slow Iran shock recovery. Nearly half of Japanese companies expect more than six months to normalize operations after the Iran conflict, citing energy disruption and Strait of Hormuz risks, according to a Reuters survey. 56% also said AI is already reshaping hiring, with weaker office demand but stronger need for AI-skilled workers. (Reuters)

- SK Hynix advances next-generation AI memory. SK Hynix (000660.KS +3.47%) has shipped samples of its latest 12-layer HBM4E chips to major customers, offering more than 20% better power efficiency and faster performance than previous models. The move strengthens its position in the AI memory market, where it is a key supplier to Nvidia (NVDA -1.33%). (Reuters) NVDA is our Core Recommendation.

- CSE Global remains supported by strong orderbook. CSE Global (CSE SP +0.04%) said its response to SGX RegCo's queries reflects board-refresh matters rather than operational issues. With a robust SGD 716 mn orderbook as of 1Q26, the company expects a softer 1H26 due to new facility start-up costs, while maintaining solid long-term growth prospects. (UOB Kay Hian Institutional Research)

EMEA and Others

- European stocks gain on trade optimism. STOXX 600 rose 0.52% on Wednesday as investors focused on signals from the G7 summit and growing optimism over a potential EU-India free trade agreement. Germany's DAX gained 0.1% and the UK's FTSE 100 added 0.14%, while France's CAC 40 slipped 0.2%. (Reuters)

- Europe pushes for AI sovereignty. Technology sovereignty is set to dominate discussions at the G7 and VivaTech this week as European policymakers seek to reduce dependence on US AI infrastructure and models. Recent US restrictions on advanced AI exports have highlighted Europe's reliance on foreign cloud, chip and AI providers, including IBM (IBM -3.12%). (Reuters)

- BMW warning highlights auto sector pressures. BMW (BMW GR -3.33%) shares fell to their lowest level since 2020 after the carmaker cut its 2026 profit outlook, citing weakness in China's auto market and pressures linked to the Iran conflict. The warning also weighed on European peers including Volkswagen (VOW GR -1.57%) and Mercedes-Benz (MBG GR -1.9%). (Reuters)

- Qatar stake complicates Volkswagen defence deal. Volkswagen (VOW GR -1.57%) is facing complications in plans to partner with Israeli defence firm Rafael at its underutilised Osnabrueck plant, as major shareholder Qatar Investment Authority has reportedly raised concerns over the discussions. The issue could delay Volkswagen's efforts to repurpose excess manufacturing capacity amid weak European auto demand. (Reuters)

- Stellantis explores new partnership opportunities. Stellantis (STLAM

IM -3.25%) is in talks with potential partners for two additional manufacturing deals in Italy, including one involving its luxury Maserati brand, as part of efforts to strengthen technology and product development. The automaker is also expanding existing collaborations with Leapmotor (9863.HK -0.82%) and Dongfeng Motor under its long-term growth strategy. (Reuters)

TRADERS’ CORNER

Source: TradingView | HBM (2142.HK)

Last Price: HK$11.22 Support Levels: HK$10.06 (-10.3%)/ HK$9.46 (-15.7%) Resistance Levels: HK$13.68 (+21.9%)/ HK$14.98 (+33.5%) |

Our Technical View

- Price action has staged a decisive rebound from a major weekly resistance-turned-support zone, validating the long-term structural floor.

- This structural defence is supported by the RSI trending upward toward the neutral 50 level.

- Provided the asset maintains its footing above this critical weekly demand floor, the current framework points toward a high-probability continuation into higher territory.

Source: TradingView | Sunny Optical (2382.HK)

Last Price: HK$79.55 Support Levels: HK$73.80 (-7.2%)/ HK$69.80 (-12.3%) Resistance Levels: HK$86.30 (+8.5%)/ HK$90.05 (+13.2%) |

Our Technical View

- Following a clean bounce off its resistance-turned-support zone, the asset has renewed its upward expansion.

- Momentum has officially shifted in favour of the bulls as the RSI clears its neutral midline and trends upward.

- Provided this underlying buying velocity persists, the path of least resistance points toward an impending challenge of the recent peak, clearing the path for further structural upside.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.