Overnight Markets

Today’s Must-Know News

S&P 500 closes in on record high as AI chip momentum broadens. S&P 500 and Nasdaq rose 0.72% & 1.12% on Monday, leaving the S&P 500 just 1.1% below its record high, as semiconductors rebounded (SOXX +2.68%). Broadcom (AVGO +3.73%) extended its Apple (AAPL +1.31%) custom ASIC supply agreement through 2031, with Apple accounting for about 20% of Broadcom’s annual revenue. SpaceX (SPCX -0.98%) slipped ahead of its Nasdaq-100 inclusion. Microsoft (MSFT -0.96%) will cut 4,800 jobs, including 3,200 Xbox roles, as it reallocates capital toward AI and higher-return businesses. Samsung (005930 KS +1.75%) fell 6.09% in early Tuesday trading despite preliminary 2Q operating profit of KRW89.4tn beating the KRW84.2tn estimate, while peer SK Hynix (000660 KS -3.18%) also dropped 2.47%. SK Hynix launched a USD28.07bn Nasdaq ADR sale, with institutional investors indicating up to USD7bn of interest. AVGO & MSFT are our Core Recommendations.

Trump eyes Xi US visit. Trump said he expects to host China’s Xi Jinping in the US around September 24, near his September 22 UN General Assembly speech and usual NY meetings with world leaders.

Trader’s Corner (Details on Page 5-6)

Ticker | Name | Rec. | Support Levels | Resistance Levels |

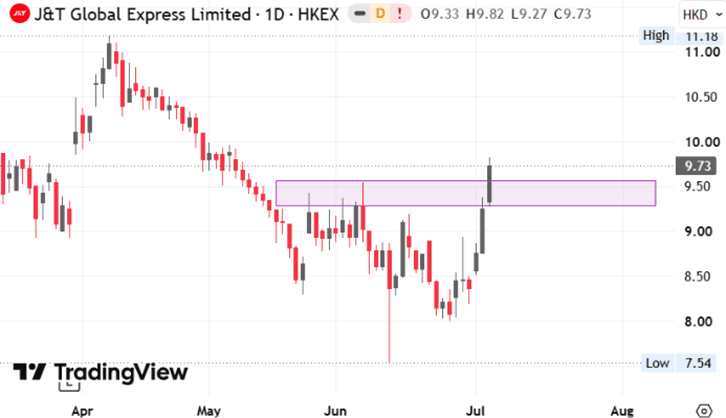

1519.HK | J&T Global Express | - | HKD 9.27 / 8.76 | HKD 10.31 / 11.25 |

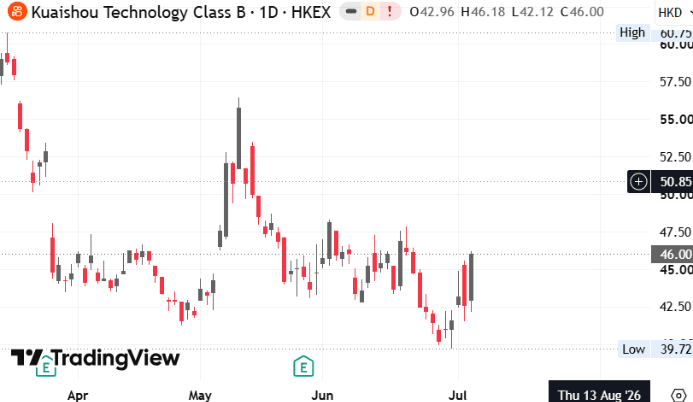

1024.HK | Kuaishou Technology | - | HKD 41.52 / 39.72 | HKD 53.50 / 57.00 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

Ticker | Company Name | Sector | IPO date |

1770.HK | DKE | Technology | Jul 8 |

6880.HK | Momenta-W | Technology | Jul 8 |

7656.HK | Reconova | Technology | Jul 8 |

7687.HK | Eacon | Consumer Disc. | Jul 8 |

8090.HK | Baogai | Industrials | Jul 8 |

9971.HK | Basic Semi | Technology | Jul 8 |

0537.HK | Rigol | Industrials | Jul 9 |

1377.HK | Dtech | Industrials | Jul 9 |

2475.HK | Luxshare ICT | Technology | Jul 9 |

2797.HK | Qiyunshan Food | Consumer Staples | Jul 9 |

3752.HK | Rokae Robotics | Industrials | Jul 9 |

6951.HK | CCTC | Technology | Jul 9 |

2249.HK | Nexchip | Technology | Jul 10 |

6745.HK | Befar Group | Materials | Jul 10 |

2523.HK | EKH | Industrials | Jul 13 |

Americas

Fed minutes to test policy tone. Fed Governor Christopher Waller said forward guidance remains useful when applied carefully, while describing Chair Kevin Warsh’s message as reaffirming the Fed’s 2% inflation commitment rather than recommitting it. The Fed’s June meeting minutes due Wednesday may offer investors more detail on officials’ inflation concerns after Warsh shortened the post-meeting statement and did not submit interest-rate projections. (Bloomberg)

Nvidia Kyber delay lifts AI alternatives. Marvell (MRVL +1.62%) rose Monday as reports that Nvidia’s (NVDA +0.37%) Kyber NVL144 AI rack architecture faced production setbacks and a delay of more than 12 months spurred investor interest in alternative AI infrastructure suppliers. The read-through potentially supports AMD (AMD +6.61%), Alphabet’s Google (GOOGL +1.82%) TPUs and optical networking names, though Nvidia said its roadmap remains intact and some analysts viewed the report as market noise. (Bloomberg) NVDA is our Core Recommendation; GOOGL is our Trading Buy.

Micron deepens auto supply. Micron (MU +0.94%) signed a long-term semiconductor supply agreement with Ford (F +3.52%) for memory and storage platforms in next-generation vehicles, days after a similar deal with General Motors (GM +2.43%). DRAM prices have risen about 70% since December as AI data-centre demand tightens supply, increasing competition from automakers using more chips in driver-assistance and infotainment systems. (Reuters) MU is our Trading Buy.

AI rotation may broaden. Morgan Stanley (MS +3.82%) said recent semiconductor weakness suggests investors may rotate from chipmakers into AI hyperscalers such as Alphabet (GOOGL +1.82%), Amazon (AMZN +0.61%) and Meta (META +2.98%), as the AI cycle shifts toward capex discipline and monetisation. The note also flagged potential support for consumer discretionary, transport and biotech stocks as Fed hike expectations ease and oil prices fall. (Reuters) AMZN & META are our Core Recommendations; GOOGL is our Trading Buy.

Walmart lowers beef prices. Walmart (WMT -1.06%) will cut prices on ground beef and other summer items after a request from the Trump administration, with one-pound 73% ground beef rolls falling about 12% to USD 5.94 from USD 6.74. The move comes as record beef prices pressure US consumers, while Trump has separately pushed low-tariff Argentine beef imports and a DOJ probe into meatpacker pricing. (Bloomberg) WMT is our Core Recommendation.

Tesla robotaxi reaches Miami. Tesla (TSLA +6.69%) rose Monday after expanding its Robotaxi service to selected parts of Miami, adding a second market after Austin. The rollout strengthens Tesla’s autonomous ride-hailing push and increases competition with Alphabet-owned Waymo (GOOGL +1.82%), though downtown Miami and Miami Beach are not yet covered. (Gurufocus) GOOGL is our Trading Buy.

CISA uses Anthropic model. The US cyber agency CISA is using Anthropic’s Mythos AI model to audit government code repositories for vulnerabilities, according to sources. The work highlights continued US government demand for Anthropic tools despite earlier tensions over Pentagon restrictions and safeguards against weapons or surveillance use. (Reuters)

Boeing 737 output ramp advances. Boeing (BA +3.55%) plans to start operating a fourth 737 MAX assembly line at its Everett factory as it works to lift production of its key single-aisle jet amid strong global aircraft demand. The new North Line comes as Boeing ramps 737 output from 42 to 47 jets per month, though it is not expected to support further rate increases before early 2027, when Boeing targets 52 jets per month. (Reuters)

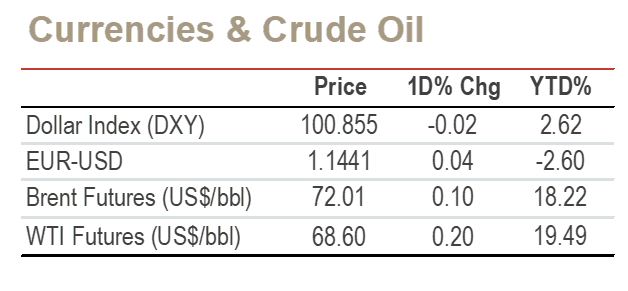

Oil oversupply signs build. The front month WTI crude futures traded near USD 69/bbl in early Tuesday as signs of global oversupply increased, with Saudi Arabia cutting its main crude price for Asian buyers and selling at a discount for the first time since its 2020 price war. At least eight Mitsui OSK-controlled ships exited the Strait of Hormuz on a route close to Iran, including some of the last trapped oil tankers to leave the waterway. (Bloomberg)

Lockheed expands naval defence portfolio. Lockheed Martin (LMT -1.45%) agreed to buy Ultra Maritime from Advent for USD 3.45 bn, adding anti-submarine warfare and undersea defence technologies as global military demand rises. Ultra Maritime will join Lockheed’s rotary and mission systems unit, which generated USD 17.3 bn revenue in 2025, amid stronger defence spending linked to Ukraine, the Middle East and the US 2027 budget request. (Reuters)

Syntiant files for AI IPO. Intel- and Microsoft-backed Syntiant filed for a Nasdaq IPO under the ticker SYTN, targeting AI demand for low-power chips and software used in earbuds, wearables and industrial devices. The company posted a wider 1Q net loss of USD 26.2mn on revenue of USD 64.5mn, while founders will retain majority voting control after listing. (Bloomberg)

Greater China

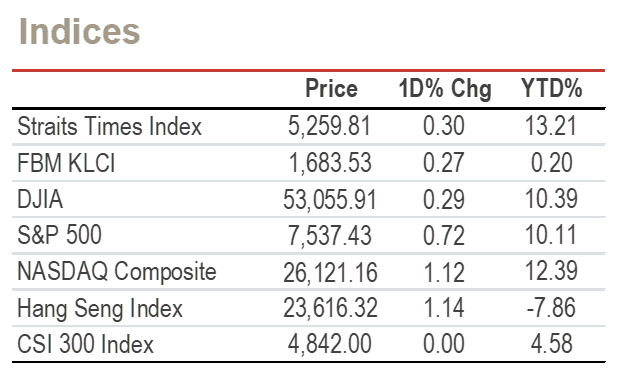

China-HK risk appetite broadens. Hong Kong stocks rose Monday as investor enthusiasm for AI broadened into other sectors, with the HSI index gaining 1.14%. However, the CSI 300 index closed nearly flat. Sentiment was supported by China’s proposed refinancing-rule changes for listed firms, new Shenzhen trading rules. Hong Kong’s June PMI rose to 52 from May's 50.4. (Reuters)

Tencent trims Kuaishou stake. Tencent’s (0700.HK +4.82%) unit Tencent Mobility is selling about 273 mn Kuaishou (1024.HK +7.98%) shares for up to USD 1.55 bn, priced at a 3.2-6.2% discount to Kuaishou’s last close. Tencent’s stake will fall to 9.37% from 15.68%, ending its status as a substantial shareholder, while Kuaishou will not receive proceeds from the secondary sale. (Reuters) 0700.HK is our Core Recommendation.

Tencent upgrades Hunyuan AI model. Tencent (0700.HK +4.82%) launched Hunyuan Hy3 with improved reasoning, agent and long-context capabilities, delivering performance comparable to larger domestic and global flagship models despite smaller parameter size. In an internal blind test across real-world productivity tasks, Hy3 scored 2.67/4 versus GLM5.1’s 2.51/4, with stronger results in frontend, data, storage and CI/CD. (AAStocks) 0700.HK is our Core Recommendation.

HSBC adds Gulf bankers. HSBC (HSBA LN +1.01; 0005.HK flat) hired three senior bankers for its Saudi Arabia capital markets and advisory team, strengthening M&A, ECM and leveraged finance coverage. The appointments support HSBC’s push into the Gulf and Middle East-Asia dealmaking corridor even as the group restructures and scales back other global operations. (Reuters) 0005.HK is our Core Recommendation.

Nvidia delay hits suppliers: Nvidia’s (NVDA +0.37%) reported Kyber NVL144 delay drove sharp selling across Asian AI hardware suppliers, including Ibiden (4062 JP -8.37%), Kingboard Laminates (1888.HK -12.55%), Elite Material (2383 TT -10%) & Samsung Electro-Mechanics (009150 KS -8.82%), as investors reassessed AI server-rack execution risk despite Nvidia saying its roadmap remains intact. (Bloomberg) NVDA is our Core Recommendation.

Luxshare prices HK listng at top. Luxshare Precision (002475.SZ -2.42%) plans to price its Hong Kong listing at HKD 63.28, raising HKD 24.3 bn (USD 3.1 bn) in the city’s largest first-time share sale this year. Trading is due to start Thursday after formal pricing later today (Tuesday). (Bloomberg)

Unimicron taps AI chip demand. Unimicron (3037.TT -5.37%) plans to raise about USD 1.4 bn from a global share sale, offering 50 mn global depositary shares at USD 26.96-27.76 each to fund foreign-currency raw material purchases. The pricing implies a 3.0-5.8% discount to its Taipei close, adding to Asian chip-related companies tapping global investors amid AI-driven semiconductor supply-chain demand. (Reuters)

Asia ex. China

Samsung wage tensions widen. Samsung (005930.KS +1.75%) appliance, smartphone and TV workers plan a July 16 rally to protest larger bonuses won by semiconductor employees. Non-chip workers are expected to receive about KRW 6 mn in treasury shares for 2026, versus up to KRW 600 mn for some chip workers. (Reuters)

Grab loses Uber board link. Grab (GRAB -1.28%) fell Monday after the Singapore-based ride-hailing and delivery company said Uber CEO Dara Khosrowshahi stepped down from its board, effective Monday. The change removes a high-profile board representative tied to Uber’s earlier strategic relationship with Grab. (Bloomberg)

EMEA and Others

Europe rally pauses after record. Europe’s STOXX 600 slipped 0.35% Monday after touching a record high, while Germany’s DAX rose 0.15% to a fresh record on stronger-than-expected German industrial orders; France’s CAC and the UK’s FTSE fell 0.33% and 0.26% respectively as investors took profit after last week’s rally. Utilities, healthcare and food-and-beverage stocks dragged, while easyJet (EZJ LN +9.28%) jumped 9.28% after agreeing in principle to Castlelake’s sweetened takeover offer valuing the airline at up to GBP 5.5 bn, or USD 7.4 bn. (Reuters)

Dutch China visit tests chips. Dutch trade minister Sjoerd Sjoerdsma will visit Beijing and Shanghai on July 7-9 as tensions persist around Nexperia’s dispute with China’s Wingtech (600745.SZ -3.84%) and potential tighter ASML (ASML NA -0.37%) export controls. The mission comes as the Netherlands pushes for coordinated restrictions rather than unilateral US-led curbs that could disproportionately hit Dutch companies. (Reuters)

- Suez return pressures shippers. Maersk (MAERSKB DC -5.45%) and Hapag-Lloyd (HLAG GR -2.39%) will resume some Gemini network sailings through the Suez Canal after security reviews, reducing Asia-Europe transit times by about four weeks. The return could pressure freight rates and shipping earnings if Red Sea stability allows broader capacity normalisation before new vessel deliveries in 2027-2028. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| J&T Global Express (1519.HK)

|

Our Technical View

Price has triggered a V-shaped breakout, penetrating its prior swing high on expansion volume.

The RSI is sustaining its trajectory above the 50-neutral threshold.

With historical overhead supply completely neutralised and trend velocity actively accelerating, the technical framework strongly favours further near-term upside.

Source: TradingView |

| Kuaishou Technology (1024.HK)

|

Our Technical View

Following a successful defence of the HK$39.72 floor, price is developing a higher low, setting the stage for an immediate retest of its overhead resistance ceiling.

The RSI has successfully crossed above the 50-neutral threshold into positive territory.

With a proven structural floor locked in underneath, the technical framework strongly favours further near-term upside.

Today’s Must-Know News

S&P 500 closes in on record high as AI chip momentum broadens. S&P 500 and Nasdaq rose 0.72% & 1.12% on Monday, leaving the S&P 500 just 1.1% below its record high, as semiconductors rebounded (SOXX +2.68%). Broadcom (AVGO +3.73%) extended its Apple (AAPL +1.31%) custom ASIC supply agreement through 2031, with Apple accounting for about 20% of Broadcom’s annual revenue. SpaceX (SPCX -0.98%) slipped ahead of its Nasdaq-100 inclusion. Microsoft (MSFT -0.96%) will cut 4,800 jobs, including 3,200 Xbox roles, as it reallocates capital toward AI and higher-return businesses. Samsung (005930 KS +1.75%) fell 6.09% in early Tuesday trading despite preliminary 2Q operating profit of KRW89.4tn beating the KRW84.2tn estimate, while peer SK Hynix (000660 KS -3.18%) also dropped 2.47%. SK Hynix launched a USD28.07bn Nasdaq ADR sale, with institutional investors indicating up to USD7bn of interest. AVGO & MSFT are our Core Recommendations.

Trump eyes Xi US visit. Trump said he expects to host China’s Xi Jinping in the US around September 24, near his September 22 UN General Assembly speech and usual NY meetings with world leaders.

Trader’s Corner (Details on Page 5-6)

Ticker | Name | Rec. | Support Levels | Resistance Levels |

1519.HK | J&T Global Express | - | HKD 9.27 / 8.76 | HKD 10.31 / 11.25 |

1024.HK | Kuaishou Technology | - | HKD 41.52 / 39.72 | HKD 53.50 / 57.00 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

Ticker | Company Name | Sector | IPO date |

1770.HK | DKE | Technology | Jul 8 |

6880.HK | Momenta-W | Technology | Jul 8 |

7656.HK | Reconova | Technology | Jul 8 |

7687.HK | Eacon | Consumer Disc. | Jul 8 |

8090.HK | Baogai | Industrials | Jul 8 |

9971.HK | Basic Semi | Technology | Jul 8 |

0537.HK | Rigol | Industrials | Jul 9 |

1377.HK | Dtech | Industrials | Jul 9 |

2475.HK | Luxshare ICT | Technology | Jul 9 |

2797.HK | Qiyunshan Food | Consumer Staples | Jul 9 |

3752.HK | Rokae Robotics | Industrials | Jul 9 |

6951.HK | CCTC | Technology | Jul 9 |

2249.HK | Nexchip | Technology | Jul 10 |

6745.HK | Befar Group | Materials | Jul 10 |

2523.HK | EKH | Industrials | Jul 13 |

Americas

Fed minutes to test policy tone. Fed Governor Christopher Waller said forward guidance remains useful when applied carefully, while describing Chair Kevin Warsh’s message as reaffirming the Fed’s 2% inflation commitment rather than recommitting it. The Fed’s June meeting minutes due Wednesday may offer investors more detail on officials’ inflation concerns after Warsh shortened the post-meeting statement and did not submit interest-rate projections. (Bloomberg)

Nvidia Kyber delay lifts AI alternatives. Marvell (MRVL +1.62%) rose Monday as reports that Nvidia’s (NVDA +0.37%) Kyber NVL144 AI rack architecture faced production setbacks and a delay of more than 12 months spurred investor interest in alternative AI infrastructure suppliers. The read-through potentially supports AMD (AMD +6.61%), Alphabet’s Google (GOOGL +1.82%) TPUs and optical networking names, though Nvidia said its roadmap remains intact and some analysts viewed the report as market noise. (Bloomberg) NVDA is our Core Recommendation; GOOGL is our Trading Buy.

Micron deepens auto supply. Micron (MU +0.94%) signed a long-term semiconductor supply agreement with Ford (F +3.52%) for memory and storage platforms in next-generation vehicles, days after a similar deal with General Motors (GM +2.43%). DRAM prices have risen about 70% since December as AI data-centre demand tightens supply, increasing competition from automakers using more chips in driver-assistance and infotainment systems. (Reuters) MU is our Trading Buy.

AI rotation may broaden. Morgan Stanley (MS +3.82%) said recent semiconductor weakness suggests investors may rotate from chipmakers into AI hyperscalers such as Alphabet (GOOGL +1.82%), Amazon (AMZN +0.61%) and Meta (META +2.98%), as the AI cycle shifts toward capex discipline and monetisation. The note also flagged potential support for consumer discretionary, transport and biotech stocks as Fed hike expectations ease and oil prices fall. (Reuters) AMZN & META are our Core Recommendations; GOOGL is our Trading Buy.

Walmart lowers beef prices. Walmart (WMT -1.06%) will cut prices on ground beef and other summer items after a request from the Trump administration, with one-pound 73% ground beef rolls falling about 12% to USD 5.94 from USD 6.74. The move comes as record beef prices pressure US consumers, while Trump has separately pushed low-tariff Argentine beef imports and a DOJ probe into meatpacker pricing. (Bloomberg) WMT is our Core Recommendation.

Tesla robotaxi reaches Miami. Tesla (TSLA +6.69%) rose Monday after expanding its Robotaxi service to selected parts of Miami, adding a second market after Austin. The rollout strengthens Tesla’s autonomous ride-hailing push and increases competition with Alphabet-owned Waymo (GOOGL +1.82%), though downtown Miami and Miami Beach are not yet covered. (Gurufocus) GOOGL is our Trading Buy.

CISA uses Anthropic model. The US cyber agency CISA is using Anthropic’s Mythos AI model to audit government code repositories for vulnerabilities, according to sources. The work highlights continued US government demand for Anthropic tools despite earlier tensions over Pentagon restrictions and safeguards against weapons or surveillance use. (Reuters)

Boeing 737 output ramp advances. Boeing (BA +3.55%) plans to start operating a fourth 737 MAX assembly line at its Everett factory as it works to lift production of its key single-aisle jet amid strong global aircraft demand. The new North Line comes as Boeing ramps 737 output from 42 to 47 jets per month, though it is not expected to support further rate increases before early 2027, when Boeing targets 52 jets per month. (Reuters)

Oil oversupply signs build. The front month WTI crude futures traded near USD 69/bbl in early Tuesday as signs of global oversupply increased, with Saudi Arabia cutting its main crude price for Asian buyers and selling at a discount for the first time since its 2020 price war. At least eight Mitsui OSK-controlled ships exited the Strait of Hormuz on a route close to Iran, including some of the last trapped oil tankers to leave the waterway. (Bloomberg)

Lockheed expands naval defence portfolio. Lockheed Martin (LMT -1.45%) agreed to buy Ultra Maritime from Advent for USD 3.45 bn, adding anti-submarine warfare and undersea defence technologies as global military demand rises. Ultra Maritime will join Lockheed’s rotary and mission systems unit, which generated USD 17.3 bn revenue in 2025, amid stronger defence spending linked to Ukraine, the Middle East and the US 2027 budget request. (Reuters)

Syntiant files for AI IPO. Intel- and Microsoft-backed Syntiant filed for a Nasdaq IPO under the ticker SYTN, targeting AI demand for low-power chips and software used in earbuds, wearables and industrial devices. The company posted a wider 1Q net loss of USD 26.2mn on revenue of USD 64.5mn, while founders will retain majority voting control after listing. (Bloomberg)

Greater China

China-HK risk appetite broadens. Hong Kong stocks rose Monday as investor enthusiasm for AI broadened into other sectors, with the HSI index gaining 1.14%. However, the CSI 300 index closed nearly flat. Sentiment was supported by China’s proposed refinancing-rule changes for listed firms, new Shenzhen trading rules. Hong Kong’s June PMI rose to 52 from May's 50.4. (Reuters)

Tencent trims Kuaishou stake. Tencent’s (0700.HK +4.82%) unit Tencent Mobility is selling about 273 mn Kuaishou (1024.HK +7.98%) shares for up to USD 1.55 bn, priced at a 3.2-6.2% discount to Kuaishou’s last close. Tencent’s stake will fall to 9.37% from 15.68%, ending its status as a substantial shareholder, while Kuaishou will not receive proceeds from the secondary sale. (Reuters) 0700.HK is our Core Recommendation.

Tencent upgrades Hunyuan AI model. Tencent (0700.HK +4.82%) launched Hunyuan Hy3 with improved reasoning, agent and long-context capabilities, delivering performance comparable to larger domestic and global flagship models despite smaller parameter size. In an internal blind test across real-world productivity tasks, Hy3 scored 2.67/4 versus GLM5.1’s 2.51/4, with stronger results in frontend, data, storage and CI/CD. (AAStocks) 0700.HK is our Core Recommendation.

HSBC adds Gulf bankers. HSBC (HSBA LN +1.01; 0005.HK flat) hired three senior bankers for its Saudi Arabia capital markets and advisory team, strengthening M&A, ECM and leveraged finance coverage. The appointments support HSBC’s push into the Gulf and Middle East-Asia dealmaking corridor even as the group restructures and scales back other global operations. (Reuters) 0005.HK is our Core Recommendation.

Nvidia delay hits suppliers: Nvidia’s (NVDA +0.37%) reported Kyber NVL144 delay drove sharp selling across Asian AI hardware suppliers, including Ibiden (4062 JP -8.37%), Kingboard Laminates (1888.HK -12.55%), Elite Material (2383 TT -10%) & Samsung Electro-Mechanics (009150 KS -8.82%), as investors reassessed AI server-rack execution risk despite Nvidia saying its roadmap remains intact. (Bloomberg) NVDA is our Core Recommendation.

Luxshare prices HK listng at top. Luxshare Precision (002475.SZ -2.42%) plans to price its Hong Kong listing at HKD 63.28, raising HKD 24.3 bn (USD 3.1 bn) in the city’s largest first-time share sale this year. Trading is due to start Thursday after formal pricing later today (Tuesday). (Bloomberg)

Unimicron taps AI chip demand. Unimicron (3037.TT -5.37%) plans to raise about USD 1.4 bn from a global share sale, offering 50 mn global depositary shares at USD 26.96-27.76 each to fund foreign-currency raw material purchases. The pricing implies a 3.0-5.8% discount to its Taipei close, adding to Asian chip-related companies tapping global investors amid AI-driven semiconductor supply-chain demand. (Reuters)

Asia ex. China

Samsung wage tensions widen. Samsung (005930.KS +1.75%) appliance, smartphone and TV workers plan a July 16 rally to protest larger bonuses won by semiconductor employees. Non-chip workers are expected to receive about KRW 6 mn in treasury shares for 2026, versus up to KRW 600 mn for some chip workers. (Reuters)

Grab loses Uber board link. Grab (GRAB -1.28%) fell Monday after the Singapore-based ride-hailing and delivery company said Uber CEO Dara Khosrowshahi stepped down from its board, effective Monday. The change removes a high-profile board representative tied to Uber’s earlier strategic relationship with Grab. (Bloomberg)

EMEA and Others

Europe rally pauses after record. Europe’s STOXX 600 slipped 0.35% Monday after touching a record high, while Germany’s DAX rose 0.15% to a fresh record on stronger-than-expected German industrial orders; France’s CAC and the UK’s FTSE fell 0.33% and 0.26% respectively as investors took profit after last week’s rally. Utilities, healthcare and food-and-beverage stocks dragged, while easyJet (EZJ LN +9.28%) jumped 9.28% after agreeing in principle to Castlelake’s sweetened takeover offer valuing the airline at up to GBP 5.5 bn, or USD 7.4 bn. (Reuters)

Dutch China visit tests chips. Dutch trade minister Sjoerd Sjoerdsma will visit Beijing and Shanghai on July 7-9 as tensions persist around Nexperia’s dispute with China’s Wingtech (600745.SZ -3.84%) and potential tighter ASML (ASML NA -0.37%) export controls. The mission comes as the Netherlands pushes for coordinated restrictions rather than unilateral US-led curbs that could disproportionately hit Dutch companies. (Reuters)

- Suez return pressures shippers. Maersk (MAERSKB DC -5.45%) and Hapag-Lloyd (HLAG GR -2.39%) will resume some Gemini network sailings through the Suez Canal after security reviews, reducing Asia-Europe transit times by about four weeks. The return could pressure freight rates and shipping earnings if Red Sea stability allows broader capacity normalisation before new vessel deliveries in 2027-2028. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| J&T Global Express (1519.HK)

|

Our Technical View

Price has triggered a V-shaped breakout, penetrating its prior swing high on expansion volume.

The RSI is sustaining its trajectory above the 50-neutral threshold.

With historical overhead supply completely neutralised and trend velocity actively accelerating, the technical framework strongly favours further near-term upside.

Source: TradingView |

| Kuaishou Technology (1024.HK)

|

Our Technical View

Following a successful defence of the HK$39.72 floor, price is developing a higher low, setting the stage for an immediate retest of its overhead resistance ceiling.

The RSI has successfully crossed above the 50-neutral threshold into positive territory.

With a proven structural floor locked in underneath, the technical framework strongly favours further near-term upside.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.