Overnight Markets

Today’s Must-Know News

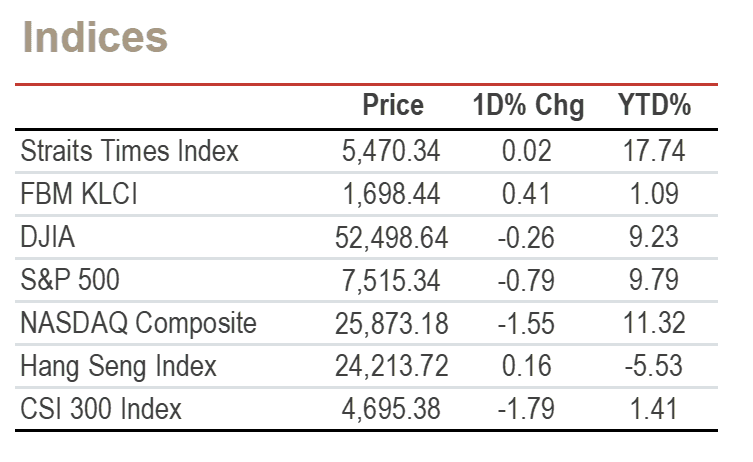

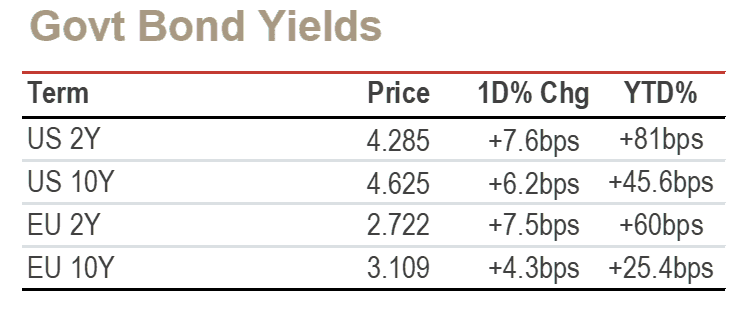

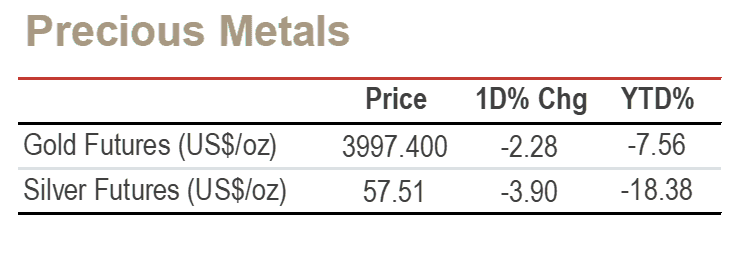

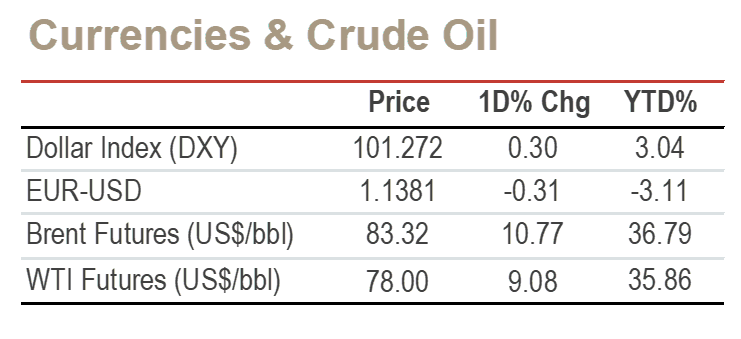

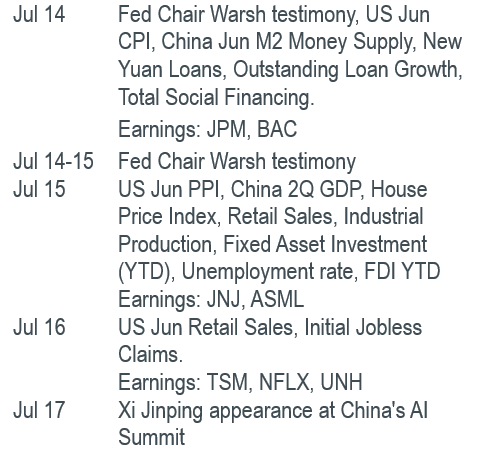

S&P 500 & Nasdaq fell 0.79% & 1.55% Monday respectively, Monday as oil-driven inflation concerns lifted Energy (XLE +3.01%) but pressured Technology & Semicon (XLK -2.42%, SOXX -4.77%) shares. The implied probability of a 25-bps July Fed rate hike rose to 43.3%, from 25.7% a week earlier, per FedWatch. Korea’s chip rout triggered a 20-minute KOSPI halt, led by SK Hynix (000660 KS -16.95%; SKHY -9.32%), while Micron (MU -4.32%), SanDisk (SNDK -12.63%) & Western Digital (WDC -4.64%). Still, SKHY retained a premium due to restricted ADR creation. J&J (JNJ +0.31%) reports 2Q26 results before-market Wednesday with options implying a 3.16% post earnings move. Investors will focus on potential guidance upgrades and the timing of late-2026 Phase 3 milvexian results. Investors are adding to Alibaba (BABA +0.02%, 9988.HK +0.45%) as the Hang Seng Tech Index rebounds 11% in two weeks and funds rotate away from Korean chipmakers. JPMorgan expects Alibaba’s June-quarter cloud revenue to grow 45%, although weak consumption and the food-delivery price war remain risks. TSMC (2330.TT +1.04%; TSM -2.89%) posted record 2Q revenue of TWD 1.27 tn, up 36% yoy, slightly above estimates, after Friday’s release was delayed. Thursday’s results are expected to show 58.8% yoy net profit growth.President Xi will deliver the opening keynote at Shanghai’s World AI Conference July 17. Front-month WTI surged >9% to USD 78.14/bbl Monday as the US reinstated its blockade of Iranian shipping from July 14 and proposed a 20% charge on cargo transiting the Strait of Hormuz. Gold (XAU -2.85%) fell below USD 4,000 intraday, while the dollar DXY +0.3%) gained. XLE, JNJ, 9988.HK & TSM are our Core Recommendations; SOXX, MU are our Trading Buys.

Trader’s Corner (Details on Page 6-7)

Ticker | Name | Rec. | Support | Resistance |

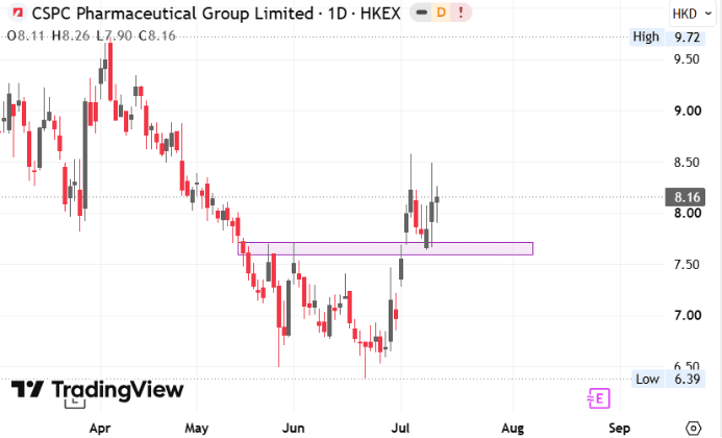

1093.HK | CSPC Pharmaceutical Group | - | HKD 7.64 / 7.28 | HKD 8.88 / 9.72 |

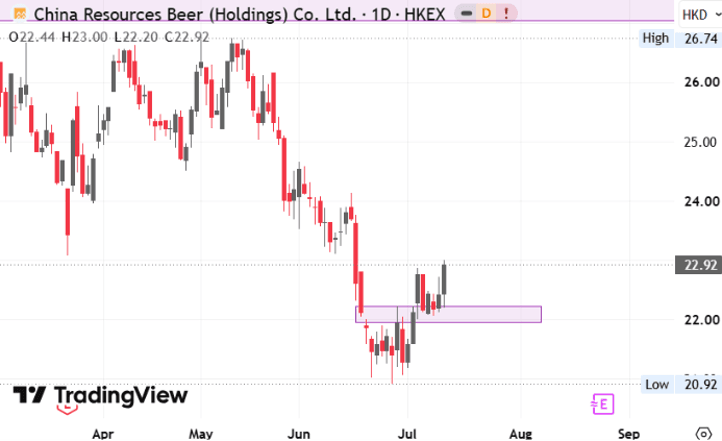

0291.HK | China Resources Beer | - | HKD 22.06 / 21.18 | HKD 24.14 / 26.70 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

Trump shifts crypto proceeds. President Trump reported more than USD 1.4 bn of crypto income in 2025 while expanding his traditional stock and bond portfolio at least fourfold to between USD 703 mn and USD 2.6 bn. His family businesses retained at least USD 160 mn in bitcoin and ether, while retail investors in four Trump-backed crypto ventures had lost an estimated USD 2.3 bn by April (Reuters)

Meta scales Hyperion investment. Meta (META -1.86%) will expand its Louisiana Hyperion data centre to 5GW from more than 2GW, lifting total investment above USD 50 bn. The firm also plans more than USD 1 bn of local infrastructure improvements and has pledged USD 600 bn for US infrastructure and jobs over three years (Reuters) META is our Core Recommendation.

Hyperscaler capex heads toward USD 1.4 tn. Morgan Stanley expects combined AI infrastructure spending by major hyperscalers to reach USD 1.4 tn in 2028 as chip, memory and networking costs rise. It forecasts Amazon (AMZN +0.8%) capex of USD 218 bn this year and USD 318 bn in 2028, alongside further spending by Alphabet (GOOGL -1.31%), Microsoft (MSFT +1.53%), Meta (META -1.86%) and SpaceX (SPCX -4.24%) (Investor’s Business Daily) AMZN, MSFT & META are our Core Recommendations; GOOGL is our Trading Buy.

Intel expands Irish AI capacity. Intel (INTC -6.12%) began a EUR 5 bn investment in Ireland to expand Intel 3 wafer capacity for AI servers and next-generation Xeon processors, with most spending scheduled by end-2027. The project represents about 30% of Intel’s planned 2026 capex and will add several hundred jobs (Reuters)

Walmart harassment claim revived. A US appeals court revived a former employee’s hostile-work-environment claim against Walmart (WMT +0.77%), ruling that a small number of severe discriminatory acts may be sufficient even without a “steady barrage” of abuse. The court upheld the dismissal of the remaining discrimination, retaliation and constructive-discharge claims (Reuters) WMT is our Core Recommendation.

US bank earnings begin Tuesday. Bank of America (BAC -0.28%) and JPMorgan (JPM -0.58%) report 2Q26 results on Tuesday, with analysts expecting BAC, JPM, Citi (C -0.06%), Goldman (GS -0.88%) and Morgan Stanley (MS -0.54%) to generate nearly USD 39 bn in combined trading revenue. Higher rates should support earnings, although credit provisions are a key risk (Reuters / Bloomberg)

Disney streaming exit could unlock value. Wells Fargo estimated Disney (DIS +0.4%) could gain 40% by exiting direct streaming and licensing its content, potentially generating more than USD 15 bn of annual revenue. Separately, the live-action Moana opened with a weaker-than-expected USD 43mn at the US and Canadian box office (Bloomberg)

Tariff refunds widen US deficit. The US recorded a USD 120 bn June budget deficit after refunding USD 49.2 bn of tariffs ruled illegal, producing a net customs outflow of USD 25.6 bn versus a USD 27 bn budget surplus a year earlier. A temporary 10% global tariff expires July 24, while the administration is preparing replacement duties targetig forced-labour enforcement and excess industrial capacity (Reuters)

Starship cleared for launch. The FAA closed its investigation into SpaceX’s (SPCX -4.24%) May Starship booster failure, clearing a 13th test flight from Texas on July 16. The mission will deploy 20 operational Starlink V3 satellites, while Starship development spending has exceeded USD 15 bn (Reuters)

California restores EV support. California approved USD 3,500 rebates for first-time buyers of new EVs costing up to USD 50,000 and USD 1,750 for qualifying used vehicles. The USD 270 mn programme partially replaces federal incentives withdrawn last year, with Tesla (TSLA -3.19%) accounting for almost half of California’s EV sales in 2025 (Reuters)

Banks accelerate AI adoption. Morgan Stanley (MS -0.54%), BNY (BNY -0.43%), UBS (UBSG SW +0.43%), Goldman Sachs (GS -0.88%), JPMorgan (JPM -0.58%) and Citi (C -0.06%) are deploying AI agents across wealth management, trading, treasury and client onboarding, while maintaining human oversight for critical decisions. A KPMG survey found 51% of banks were piloting AI agents, with investors increasingly focused on returns from technology spending (Reuters)

States challenge media megadeal. California and 11 other US states sued to block Paramount’s (PSKY +1.49%) USD 110 bn acquisition of Warner Bros. Discovery (WBD +1.88%), arguing the combination could raise prices and reduce competition in film and television. Paramount may owe shareholders about USD 650mn per quarter if completion slips beyond October (Reuters)

Mastercard reviews Vocalink sale. Mastercard (MA +2.08%) is reportedly considering selling a 51% stake in UK payments operator Vocalink to British banks for about GBP 400 mn. Vocalink processes more than 90% of UK salaries and 98% of state benefits, making its US ownership a growing policy concern (Reuters)

L3Harris wins Golden Dome satellite order. L3Harris Technologies (LHX -0.72%) secured a USD 955 mn contract from the US Space Development Agency to build 18 missile-tracking satellites for the Golden Dome defence shield, taking its total US orders to at least 70 satellites. Production will begin immediately as the firm expands domestic space-manufacturing capacity. (Reuters)

AI cyber risks intensify. Canada’s financial regulator warned that Anthropic’s Claude Mythos could accelerate cyberattacks and shorten banks’ response time, prompting lenders to strengthen AI-based defences. (Reuters)

Greater China

US-Iran tensions pressure China equities. The CSI 300 fell 1.79% to a one-month low on Monday, while the HSI edged up 0.16%, as escalating US-Iran tensions, weak domestic demand and profit-taking weighed on sentiment. Blue chips are expected to retain a relative advantage during market corrections because of their defensive characteristics. (Reuters)

Xi elevates China’s flagship AI summit. President Xi Jinping will deliver the opening keynote at Shanghai’s World AI Conference on July 17, his first appearance at the event as US-China competition over AI models and global standards intensifies. Alibaba (BABA +0.02%, 9988.HK +0.45%) and other Chinese developers are racing to challenge leading US models. (Bloomberg) 9988.HK is our Core Recommendation.

AI demand drives record TSMC revenue. TSMC (2330.TT +1.04%; TSM -2.89%) reported record 2Q revenue of TWD 1.27 tn, up 36% YoY and slightly above estimates, as AI demand accelerated; June revenue jumped 67.9% YoY to TWD 442.68 bn. The Nvidia (NVDA -3.52%) and Apple (AAPL +0.63%) supplier will report earnings on Thursday, with net profit expected to rise 58.8% YoY. (Reuters) TSM & NVDA are our Core Recommendations.

TSMC expands advanced packaging capacity. TSMC (2330.TT +1.04%; TSM -2.89%) will add two advanced chip-packaging plants at Chiayi Science Park, expanding the site to four facilities as AI-related demand continues to outstrip supply. The hub is expected to generate more than TWD 300 bn in annual output and create over 9,000 jobs once fully operational. (Reuters) TSM is our Core Recommendation.

Shein advances Hong Kong IPO. Shein is scheduled for a Hong Kong listing hearing Thursday and could raise USD 2-3 bn as early as August after receiving Chinese regulatory approval, although other sources indicated a September-October listing at a USD 40-50 bn valuation. Executive Chairman Donald Tang is expected to step down into an advisory role, with founder Sky Xu likely to lead the investor roadshow. (Reuters)

Huawei expands clean-energy footprint. Huawei’s USD 11 bn digital-power business is opening new markets through battery storage and solar-inverter projects, including a major installation in Brazil, after posting double-digit revenue growth last year. The company is also exploring ways to monetise the unit, including a previously considered sale to CATL (300750.SZ +2.95%). (Bloomberg) 300750.SZ is our Core recommendation.

Smartphone shipments hit 13-year low. Global smartphone shipments fell 11% in 2Q as memory shortages raised handset prices, although Apple (AAPL +0.63%) achieved a record 20% market share and Samsung (005930 KS -10.12%) reclaimed first place with 24%. Xiaomi (1810.HK flat) and other mass-market vendors recorded sharper shipment declines, with the shortage expected to persist into 2027. (Reuters)

China growth expected to slow. China’s 2Q GDP growth is forecast to ease to 4.5% from 5% in 1Q as weak consumption and private investment offset resilient exports. Economists expect 2026 growth of 4.6%, with fiscal support likely to increase and a possible 20-bps reserve-requirement cut in 4Q. (Reuters)

Tariff front-loading supports China exports. China’s June exports are forecast to rise 18.2% YoY and imports 24%, with AI-related trade offsetting weak domestic demand. US retailers advanced orders by four to six weeks ahead of expected tariff increases, helping lift the projected trade surplus to USD 120.6 bn (Reuters)

Asia ex. China

Keppel fills Bifrost capacity. Keppel (KEP SP +0.96%) secured a hyperscaler customer for the final fibre pair on its Bifrost subsea cable, raising the estimated value of all five contracts to USD 1.3 bn. The Singapore-US system is expected to generate an internal rate of return of about 30%, while Keppel is evaluating two additional Asian cable routes. (Reuters)

DBS crosses SGD 200 bn valuation. DBS (DBS SP +0.48%) became the first Singapore-listed firm to close above SGD 200 bn in market value, with its shares reaching a record SGD 70.80 intraday. The stock has gained about 26% this year ahead of 2Q results on August 6. (Reuters)

EMEA and Others

US-Iran tensions keep Europe mixed. The STOXX 600 was down slightly by 0.01% on Monday as renewed US-Iran tensions weakened risk appetite and pressured technology stocks, outweighing gains in energy shares from the 4.8% rise in oil prices. Germany’s DAX, France’s CAC 40, and the UK’s FTSE 100 edged higher by 0.19%. 0.31%, and 0.01% respectively as stronger energy stocks offset technology weakness. Investors remained cautious ahead of the upcoming earnings season. (Reuters)

Deutsche Bank fined in Australia. Deutsche Bank (DBK GR -1.4%) paid a USD 1.3 mn penalty after Australia’s securities regulator identified inaccurate reporting across more than 260,000 derivatives transactions. The regulator described the failures as systemic, while the bank is implementing remedial measures. (Reuters)

Mercedes expands low-cost production. Mercedes-Benz (MBG GR +0.12%) invested EUR 1bn to double output at its Kecskemet plant, which will become its largest European factory and produce the electric C-Class, GLC and small G-Class. Annual capacity will rise to 350,000 vehicles and employment will increase by 3,000. (Reuters)

Volkswagen weighs deeper job cuts. Volkswagen (VOW GR +0.83%) may cut another 50,000 jobs, taking potential reductions to 100,000, as it seeks to close a 20% cost disadvantage versus rivals. Profits have been hit by tariff costs, intense China competition and pressure to improve German manufacturing efficiency, while labour representatives have rejected the restructuring plan. (Reuters)

Hapag-Lloyd raises guidance. Hapag-Lloyd (HLAG GR +6.62%) lifted its 2026 EBITDA forecast to USD 2.7-3.7 bn from USD 1.1-3.1 bn and projected EBIT of USD 100 mn-1.1 bn on stronger demand and freight rates. The outlook remains highly uncertain because of volatile shipping rates and geopolitical risks. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| CSPC Pharmaceutical Group (1093.HK)

|

Our Technical View

Price rebounded from its resistance-turned-support zone, successfully keeping the bullish price trend intact.

The RSI is rising cleanly above its 50-neutral baseline into positive territory.

Further upside extensions remain strictly contingent on a confirmed breakout above its overhead supply zone.

Source: TradingView |

| China Resources Beer (0291.HK)

|

Our Technical View

Price further penetrated its recent price high after executing a high-conviction rebound from its validated resistance-turned-support zone.

The RSI is rising cleanly above its 50-neutral baseline into a dominant bullish regime.

These support the technical framework for a sustained move higher.

Today’s Must-Know News

S&P 500 & Nasdaq fell 0.79% & 1.55% Monday respectively, Monday as oil-driven inflation concerns lifted Energy (XLE +3.01%) but pressured Technology & Semicon (XLK -2.42%, SOXX -4.77%) shares. The implied probability of a 25-bps July Fed rate hike rose to 43.3%, from 25.7% a week earlier, per FedWatch. Korea’s chip rout triggered a 20-minute KOSPI halt, led by SK Hynix (000660 KS -16.95%; SKHY -9.32%), while Micron (MU -4.32%), SanDisk (SNDK -12.63%) & Western Digital (WDC -4.64%). Still, SKHY retained a premium due to restricted ADR creation. J&J (JNJ +0.31%) reports 2Q26 results before-market Wednesday with options implying a 3.16% post earnings move. Investors will focus on potential guidance upgrades and the timing of late-2026 Phase 3 milvexian results. Investors are adding to Alibaba (BABA +0.02%, 9988.HK +0.45%) as the Hang Seng Tech Index rebounds 11% in two weeks and funds rotate away from Korean chipmakers. JPMorgan expects Alibaba’s June-quarter cloud revenue to grow 45%, although weak consumption and the food-delivery price war remain risks. TSMC (2330.TT +1.04%; TSM -2.89%) posted record 2Q revenue of TWD 1.27 tn, up 36% yoy, slightly above estimates, after Friday’s release was delayed. Thursday’s results are expected to show 58.8% yoy net profit growth.President Xi will deliver the opening keynote at Shanghai’s World AI Conference July 17. Front-month WTI surged >9% to USD 78.14/bbl Monday as the US reinstated its blockade of Iranian shipping from July 14 and proposed a 20% charge on cargo transiting the Strait of Hormuz. Gold (XAU -2.85%) fell below USD 4,000 intraday, while the dollar DXY +0.3%) gained. XLE, JNJ, 9988.HK & TSM are our Core Recommendations; SOXX, MU are our Trading Buys.

Trader’s Corner (Details on Page 6-7)

Ticker | Name | Rec. | Support | Resistance |

1093.HK | CSPC Pharmaceutical Group | - | HKD 7.64 / 7.28 | HKD 8.88 / 9.72 |

0291.HK | China Resources Beer | - | HKD 22.06 / 21.18 | HKD 24.14 / 26.70 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

Trump shifts crypto proceeds. President Trump reported more than USD 1.4 bn of crypto income in 2025 while expanding his traditional stock and bond portfolio at least fourfold to between USD 703 mn and USD 2.6 bn. His family businesses retained at least USD 160 mn in bitcoin and ether, while retail investors in four Trump-backed crypto ventures had lost an estimated USD 2.3 bn by April (Reuters)

Meta scales Hyperion investment. Meta (META -1.86%) will expand its Louisiana Hyperion data centre to 5GW from more than 2GW, lifting total investment above USD 50 bn. The firm also plans more than USD 1 bn of local infrastructure improvements and has pledged USD 600 bn for US infrastructure and jobs over three years (Reuters) META is our Core Recommendation.

Hyperscaler capex heads toward USD 1.4 tn. Morgan Stanley expects combined AI infrastructure spending by major hyperscalers to reach USD 1.4 tn in 2028 as chip, memory and networking costs rise. It forecasts Amazon (AMZN +0.8%) capex of USD 218 bn this year and USD 318 bn in 2028, alongside further spending by Alphabet (GOOGL -1.31%), Microsoft (MSFT +1.53%), Meta (META -1.86%) and SpaceX (SPCX -4.24%) (Investor’s Business Daily) AMZN, MSFT & META are our Core Recommendations; GOOGL is our Trading Buy.

Intel expands Irish AI capacity. Intel (INTC -6.12%) began a EUR 5 bn investment in Ireland to expand Intel 3 wafer capacity for AI servers and next-generation Xeon processors, with most spending scheduled by end-2027. The project represents about 30% of Intel’s planned 2026 capex and will add several hundred jobs (Reuters)

Walmart harassment claim revived. A US appeals court revived a former employee’s hostile-work-environment claim against Walmart (WMT +0.77%), ruling that a small number of severe discriminatory acts may be sufficient even without a “steady barrage” of abuse. The court upheld the dismissal of the remaining discrimination, retaliation and constructive-discharge claims (Reuters) WMT is our Core Recommendation.

US bank earnings begin Tuesday. Bank of America (BAC -0.28%) and JPMorgan (JPM -0.58%) report 2Q26 results on Tuesday, with analysts expecting BAC, JPM, Citi (C -0.06%), Goldman (GS -0.88%) and Morgan Stanley (MS -0.54%) to generate nearly USD 39 bn in combined trading revenue. Higher rates should support earnings, although credit provisions are a key risk (Reuters / Bloomberg)

Disney streaming exit could unlock value. Wells Fargo estimated Disney (DIS +0.4%) could gain 40% by exiting direct streaming and licensing its content, potentially generating more than USD 15 bn of annual revenue. Separately, the live-action Moana opened with a weaker-than-expected USD 43mn at the US and Canadian box office (Bloomberg)

Tariff refunds widen US deficit. The US recorded a USD 120 bn June budget deficit after refunding USD 49.2 bn of tariffs ruled illegal, producing a net customs outflow of USD 25.6 bn versus a USD 27 bn budget surplus a year earlier. A temporary 10% global tariff expires July 24, while the administration is preparing replacement duties targetig forced-labour enforcement and excess industrial capacity (Reuters)

Starship cleared for launch. The FAA closed its investigation into SpaceX’s (SPCX -4.24%) May Starship booster failure, clearing a 13th test flight from Texas on July 16. The mission will deploy 20 operational Starlink V3 satellites, while Starship development spending has exceeded USD 15 bn (Reuters)

California restores EV support. California approved USD 3,500 rebates for first-time buyers of new EVs costing up to USD 50,000 and USD 1,750 for qualifying used vehicles. The USD 270 mn programme partially replaces federal incentives withdrawn last year, with Tesla (TSLA -3.19%) accounting for almost half of California’s EV sales in 2025 (Reuters)

Banks accelerate AI adoption. Morgan Stanley (MS -0.54%), BNY (BNY -0.43%), UBS (UBSG SW +0.43%), Goldman Sachs (GS -0.88%), JPMorgan (JPM -0.58%) and Citi (C -0.06%) are deploying AI agents across wealth management, trading, treasury and client onboarding, while maintaining human oversight for critical decisions. A KPMG survey found 51% of banks were piloting AI agents, with investors increasingly focused on returns from technology spending (Reuters)

States challenge media megadeal. California and 11 other US states sued to block Paramount’s (PSKY +1.49%) USD 110 bn acquisition of Warner Bros. Discovery (WBD +1.88%), arguing the combination could raise prices and reduce competition in film and television. Paramount may owe shareholders about USD 650mn per quarter if completion slips beyond October (Reuters)

Mastercard reviews Vocalink sale. Mastercard (MA +2.08%) is reportedly considering selling a 51% stake in UK payments operator Vocalink to British banks for about GBP 400 mn. Vocalink processes more than 90% of UK salaries and 98% of state benefits, making its US ownership a growing policy concern (Reuters)

L3Harris wins Golden Dome satellite order. L3Harris Technologies (LHX -0.72%) secured a USD 955 mn contract from the US Space Development Agency to build 18 missile-tracking satellites for the Golden Dome defence shield, taking its total US orders to at least 70 satellites. Production will begin immediately as the firm expands domestic space-manufacturing capacity. (Reuters)

AI cyber risks intensify. Canada’s financial regulator warned that Anthropic’s Claude Mythos could accelerate cyberattacks and shorten banks’ response time, prompting lenders to strengthen AI-based defences. (Reuters)

Greater China

US-Iran tensions pressure China equities. The CSI 300 fell 1.79% to a one-month low on Monday, while the HSI edged up 0.16%, as escalating US-Iran tensions, weak domestic demand and profit-taking weighed on sentiment. Blue chips are expected to retain a relative advantage during market corrections because of their defensive characteristics. (Reuters)

Xi elevates China’s flagship AI summit. President Xi Jinping will deliver the opening keynote at Shanghai’s World AI Conference on July 17, his first appearance at the event as US-China competition over AI models and global standards intensifies. Alibaba (BABA +0.02%, 9988.HK +0.45%) and other Chinese developers are racing to challenge leading US models. (Bloomberg) 9988.HK is our Core Recommendation.

AI demand drives record TSMC revenue. TSMC (2330.TT +1.04%; TSM -2.89%) reported record 2Q revenue of TWD 1.27 tn, up 36% YoY and slightly above estimates, as AI demand accelerated; June revenue jumped 67.9% YoY to TWD 442.68 bn. The Nvidia (NVDA -3.52%) and Apple (AAPL +0.63%) supplier will report earnings on Thursday, with net profit expected to rise 58.8% YoY. (Reuters) TSM & NVDA are our Core Recommendations.

TSMC expands advanced packaging capacity. TSMC (2330.TT +1.04%; TSM -2.89%) will add two advanced chip-packaging plants at Chiayi Science Park, expanding the site to four facilities as AI-related demand continues to outstrip supply. The hub is expected to generate more than TWD 300 bn in annual output and create over 9,000 jobs once fully operational. (Reuters) TSM is our Core Recommendation.

Shein advances Hong Kong IPO. Shein is scheduled for a Hong Kong listing hearing Thursday and could raise USD 2-3 bn as early as August after receiving Chinese regulatory approval, although other sources indicated a September-October listing at a USD 40-50 bn valuation. Executive Chairman Donald Tang is expected to step down into an advisory role, with founder Sky Xu likely to lead the investor roadshow. (Reuters)

Huawei expands clean-energy footprint. Huawei’s USD 11 bn digital-power business is opening new markets through battery storage and solar-inverter projects, including a major installation in Brazil, after posting double-digit revenue growth last year. The company is also exploring ways to monetise the unit, including a previously considered sale to CATL (300750.SZ +2.95%). (Bloomberg) 300750.SZ is our Core recommendation.

Smartphone shipments hit 13-year low. Global smartphone shipments fell 11% in 2Q as memory shortages raised handset prices, although Apple (AAPL +0.63%) achieved a record 20% market share and Samsung (005930 KS -10.12%) reclaimed first place with 24%. Xiaomi (1810.HK flat) and other mass-market vendors recorded sharper shipment declines, with the shortage expected to persist into 2027. (Reuters)

China growth expected to slow. China’s 2Q GDP growth is forecast to ease to 4.5% from 5% in 1Q as weak consumption and private investment offset resilient exports. Economists expect 2026 growth of 4.6%, with fiscal support likely to increase and a possible 20-bps reserve-requirement cut in 4Q. (Reuters)

Tariff front-loading supports China exports. China’s June exports are forecast to rise 18.2% YoY and imports 24%, with AI-related trade offsetting weak domestic demand. US retailers advanced orders by four to six weeks ahead of expected tariff increases, helping lift the projected trade surplus to USD 120.6 bn (Reuters)

Asia ex. China

Keppel fills Bifrost capacity. Keppel (KEP SP +0.96%) secured a hyperscaler customer for the final fibre pair on its Bifrost subsea cable, raising the estimated value of all five contracts to USD 1.3 bn. The Singapore-US system is expected to generate an internal rate of return of about 30%, while Keppel is evaluating two additional Asian cable routes. (Reuters)

DBS crosses SGD 200 bn valuation. DBS (DBS SP +0.48%) became the first Singapore-listed firm to close above SGD 200 bn in market value, with its shares reaching a record SGD 70.80 intraday. The stock has gained about 26% this year ahead of 2Q results on August 6. (Reuters)

EMEA and Others

US-Iran tensions keep Europe mixed. The STOXX 600 was down slightly by 0.01% on Monday as renewed US-Iran tensions weakened risk appetite and pressured technology stocks, outweighing gains in energy shares from the 4.8% rise in oil prices. Germany’s DAX, France’s CAC 40, and the UK’s FTSE 100 edged higher by 0.19%. 0.31%, and 0.01% respectively as stronger energy stocks offset technology weakness. Investors remained cautious ahead of the upcoming earnings season. (Reuters)

Deutsche Bank fined in Australia. Deutsche Bank (DBK GR -1.4%) paid a USD 1.3 mn penalty after Australia’s securities regulator identified inaccurate reporting across more than 260,000 derivatives transactions. The regulator described the failures as systemic, while the bank is implementing remedial measures. (Reuters)

Mercedes expands low-cost production. Mercedes-Benz (MBG GR +0.12%) invested EUR 1bn to double output at its Kecskemet plant, which will become its largest European factory and produce the electric C-Class, GLC and small G-Class. Annual capacity will rise to 350,000 vehicles and employment will increase by 3,000. (Reuters)

Volkswagen weighs deeper job cuts. Volkswagen (VOW GR +0.83%) may cut another 50,000 jobs, taking potential reductions to 100,000, as it seeks to close a 20% cost disadvantage versus rivals. Profits have been hit by tariff costs, intense China competition and pressure to improve German manufacturing efficiency, while labour representatives have rejected the restructuring plan. (Reuters)

Hapag-Lloyd raises guidance. Hapag-Lloyd (HLAG GR +6.62%) lifted its 2026 EBITDA forecast to USD 2.7-3.7 bn from USD 1.1-3.1 bn and projected EBIT of USD 100 mn-1.1 bn on stronger demand and freight rates. The outlook remains highly uncertain because of volatile shipping rates and geopolitical risks. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| CSPC Pharmaceutical Group (1093.HK)

|

Our Technical View

Price rebounded from its resistance-turned-support zone, successfully keeping the bullish price trend intact.

The RSI is rising cleanly above its 50-neutral baseline into positive territory.

Further upside extensions remain strictly contingent on a confirmed breakout above its overhead supply zone.

Source: TradingView |

| China Resources Beer (0291.HK)

|

Our Technical View

Price further penetrated its recent price high after executing a high-conviction rebound from its validated resistance-turned-support zone.

The RSI is rising cleanly above its 50-neutral baseline into a dominant bullish regime.

These support the technical framework for a sustained move higher.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.